A familiar version of this problem lands on leadership desks all the time. You want an employee to receive a meaningful payment, maybe a relocation stipend, a signing bonus, or a severance amount, and then payroll points out that the employee won't receive that amount after taxes. At that point, the main question isn't just how to run the math. It's whether a gross-up is the right policy choice at all.

For employers, tax gross up decisions sit at the intersection of payroll mechanics, employee relations, and risk control. Used well, they preserve a promised value and avoid awkward surprises. Used poorly, they create hidden cost, inconsistent treatment, and documentation problems that are hard to defend later.

A common scenario goes like this. A company tells a new hire, “We'll provide a relocation payment so you have a set amount in hand to make the move work.” Then payroll reminds everyone that the payment is taxable. The employee hears one number, but their bank account reflects less.

That gap is where a tax gross up comes in. As Paylocity explains in its gross-up overview, a tax gross-up is the reverse of a standard payroll calculation. Instead of starting with gross pay and subtracting taxes, the employer starts with a target net amount and works backward to determine the higher gross payment needed so the employee still receives the intended take-home amount after withholding.

The practical purpose is simple. You're trying to protect the employee from tax erosion on a payment that was meant to deliver a specific value.

This often matters most for one-time compensation items such as:

A gross-up is less about generosity than precision. It answers one specific question: what must the employer pay so the employee receives the amount leadership intended?

A gross-up isn't the same thing as paying “more.” It's a targeted payroll method tied to a net outcome. That distinction matters because leaders often approve a benefit in principle without realizing the payroll cost will exceed the headline number.

It also isn't a substitute for broader compensation planning. If a payment connects to executive pay design, bonus timing, or deferred arrangements, it needs to fit the larger reward strategy and documentation framework. That's one reason it helps to understand how these decisions connect to broader deferred compensation concepts before promising specific net amounts.

Standard payroll asks, “What does the employee keep after taxes?” A gross-up asks, “What must we pay so the employee keeps this exact amount?”

That sounds straightforward. In practice, it becomes a policy choice with cost, tax, and communication consequences, especially once different tax layers and employee-specific variables enter the picture.

A leadership team approves a $10,000 relocation payment because they want the employee to receive the full $10,000 of value. Payroll treats it as a standard taxable payment, withholding applies, and the employee receives less than expected. The math is fixable. The harder problem is avoiding a policy failure that could have been prevented before anyone named a number.

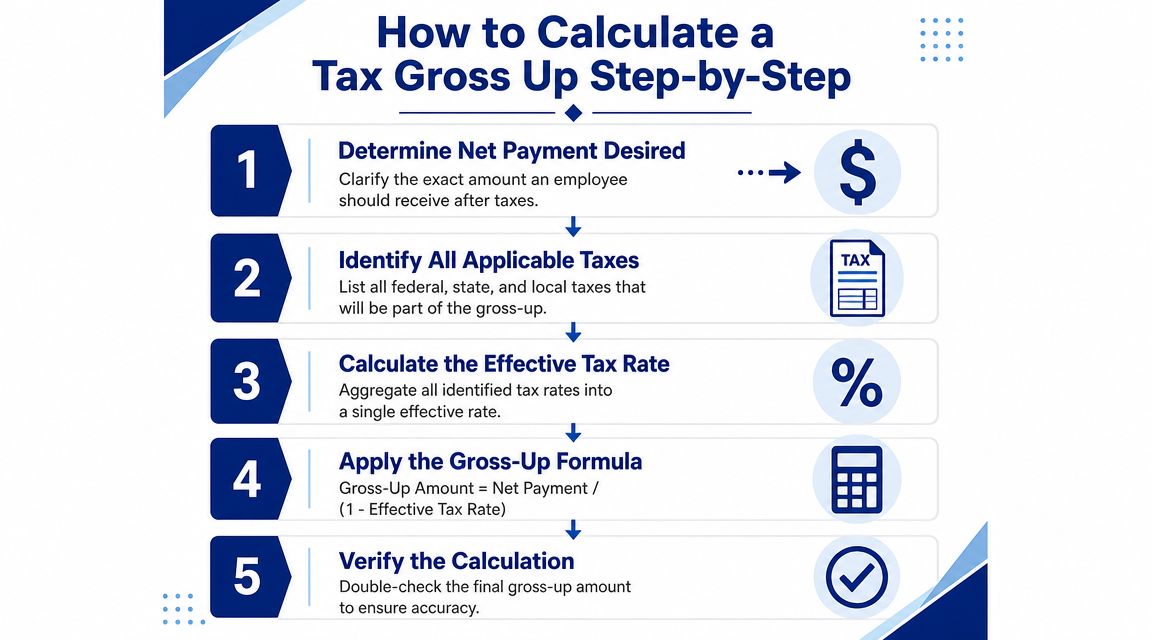

Gross-up math starts with reverse payroll. The company defines the net amount the employee should keep, then calculates the gross amount needed to support that result after withholding. A commonly used formula is Gross Pay = Net Pay / (1 - Total Tax Rate). For example, using a 25% combined tax rate, a payment of about $1,333.33 would be needed to produce $1,000 net, as outlined in Paylocity's gross-up glossary entry.

Before anyone runs numbers, define what the company is promising.

That means answering two questions clearly. Is the business committing to a specific employee net outcome, or is it approving a taxable payment amount? And is the reason for the payment strong enough to justify the added employer cost and administrative complexity?

Those questions matter because a gross-up should be a deliberate exception, not a default habit. If leadership only wants to provide support and can tolerate some employee tax impact, a flat taxable allowance may be easier to budget, easier to explain, and easier to apply consistently. If leadership wants the employee to receive an exact value for a business reason, the gross-up approach is more defensible.

Once the policy choice is clear, the calculation itself is straightforward. The control points around it are where employers usually make mistakes.

Use this sequence:

This sequence protects two things at once: the employee outcome and the company's ability to defend why it chose a gross-up in the first place.

The arithmetic looks clean. Real payroll rarely is.

Gross-ups can be affected by supplemental wage treatment, jurisdiction-specific withholding, and employee-specific factors that make a rough blended rate unreliable. That is why I do not recommend treating a spreadsheet as the final instruction for a high-visibility payment. The estimate may be directionally right and still produce the wrong deposit amount.

A better practice is to have payroll, or your payroll provider, test the transaction in the system that will process it. If your team outsources that work, align the calculation and approval steps with your managed payroll service process before anyone communicates a guaranteed net figure.

Suppose the company wants an employee to receive $1,000 net from a one-time taxable payment and uses a 25% total tax rate assumption.

The employee would net about $1,000, assuming the withholding setup matches the assumptions used in the calculation.

That final condition is where employers should slow down. The formula answers the math question. It does not confirm that the tax treatment is complete, that the earning code is correct, or that the result fits the company's stated policy.

For business leaders, the hardest part is usually alignment, not arithmetic.

If HR promises a net outcome without checking payroll treatment, the employee may feel underpaid. If finance approves a gross-up without defining when that exception is allowed, similar requests tend to follow. If managers use gross-ups inconsistently, the issue shifts from payroll mechanics to fairness and governance.

The strongest approach is to calculate only after the company has documented three points: why this payment warrants a gross-up, what net result is being promised, and who has authority to approve the extra employer cost. That is what turns a gross-up from a one-off calculation into a defensible business practice.

Not every taxable payment deserves a gross-up. The best use cases are the ones where the business has a clear reason to preserve a specific employee value and can explain why that exception makes sense.

A gross-up is often justified when the payment is meant to remove friction, not create it.

Consider these situations:

Some payments don't warrant the extra complexity.

A gross-up is often a poor fit when:

If you can't explain why this payment should be protected from tax impact while similar payments are not, you probably don't have a durable gross-up policy.

Before approving a gross-up, ask four questions:

| Question | Why it matters |

|---|---|

| Is the company promising a specific net outcome? | Gross-ups are built for net promises, not vague goodwill. |

| Would taxation undercut the business purpose of the payment? | If yes, a gross-up may preserve the intended effect. |

| Can the same rule be applied consistently? | Consistency protects fairness and defensibility. |

| Is there a simpler alternative? | A taxable allowance or redesigned benefit may work better. |

Many organizations find themselves in trouble. They treat gross-ups as a courtesy rather than as a policy decision. Once that happens, exceptions multiply, managers improvise, and payroll becomes the cleanup function.

A gross-up doesn't stop with the employee's withholding. It changes the employer's payroll picture too, because the grossed-up amount becomes part of taxable wages and has to be processed with the same discipline as any other compensation item.

The compliance environment is large and unforgiving. In an Ogletree analysis discussing IRS treatment of gross-up issues, the IRS reported that in Fiscal Year 2024 it collected more than $5.1 trillion in gross taxes, processed more than 266.6 million tax returns and other forms, and issued nearly $490.6 billion in refunds, underscoring the scale in which payroll tax decisions operate, as described in this Ogletree article on IRS gross-up clarification.

Leaders often focus on what the employee receives. Finance and payroll have to focus on what the company owes as a result of the payment structure.

That means a gross-up can affect:

A small policy decision can become a disproportionate administrative burden if the organization doesn't standardize how these payments are approved and processed.

Multi-state operations introduce another layer of risk because withholding and tax treatment can vary by employee location and work pattern. That makes one-size-fits-all gross-up assumptions especially dangerous.

Some employers try to solve this by using a standard approach for every employee. That can simplify internal administration, but it can also distort cost and create inconsistent employee outcomes. The better approach is usually to define when gross-up applies, then require payroll validation based on the employee's actual facts.

Multi-state gross-ups are less about calculator skill and more about control. The organization needs a rule for who approves them, how payroll validates them, and how exceptions are documented.

That's also why gross-up decisions should sit near broader wage and hour compliance guidance. Once an employer starts making special payments across jurisdictions, documentation discipline matters as much as the tax math.

The Ogletree discussion also noted an IRS-related case in which an employer's 2018 payment of taxes that should have been withheld on 2016 wages did not create additional 2016 wages, so no gross-up was required for that earlier year. But the same analysis pointed to a possible gross-up issue in 2018 if the later tax payment itself counted as additional wages.

That doesn't mean every employer needs to master tax controversy analysis. It does mean timing, wage characterization, and year-specific treatment can matter more than executives expect.

A relocation package gets approved at the offer stage. The business wants the employee to receive a specific net amount, but payroll has to turn that promise into taxable wages without creating a bigger problem than the one leadership was trying to solve. That is where gross-ups help, and where they often get overused.

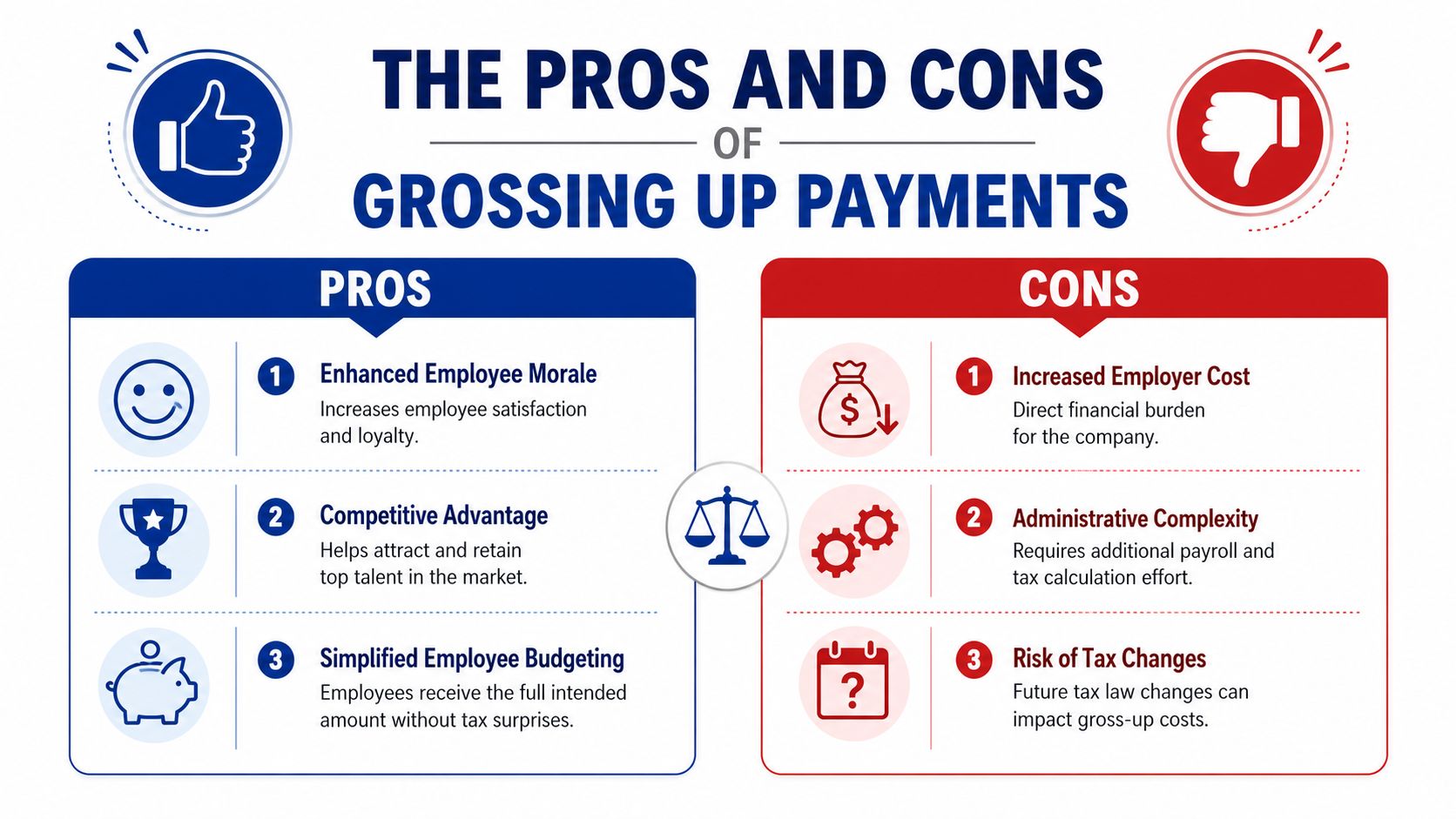

Gross-ups work best when the company is protecting a defined employee outcome tied to a legitimate business purpose. They are often effective in relocation, certain severance arrangements, and selected executive benefits where a tax reduction would undermine the value of the payment. In those cases, a gross-up can reduce disputes, support a clean employee communication, and make the employer's promise easier to honor in practice.

They also create costs that leaders do not always see at approval time.

The obvious cost is the extra pay needed to cover taxes. The less obvious cost is operational. Payroll has to code the payment correctly, HR has to document why this exception fits policy, and managers have to avoid describing it loosely as the company “covering taxes” without defining the scope. If any of those steps are weak, the payment can become harder to defend internally and harder to explain later.

By this point, the harder question is no longer how a gross-up works or whether an allowance might sometimes be better. That framework belongs earlier in the decision process. At this stage, leadership should test whether the proposed gross-up can be defended as a limited policy exception with a clear business reason, known cost, and documented approval.

This is the central policy decision for leadership.

A useful rule is simple. If the company would struggle to explain why the employee needed a guaranteed net payment, the gross-up probably does not belong in the policy. If the rationale is solid and the payment category is narrow, the gross-up may be justified even with the extra cost and payroll effort.

What fails in practice is informal pattern-setting. One manager adds a gross-up to close a hire. Another offers one to resolve a complaint. Soon the organization has an unwritten benefit practice that payroll has to clean up after the fact. That is usually where fairness concerns, inconsistent treatment, and avoidable compliance exposure start.

Most gross-up problems don't start with tax law. They start with loose promises, inconsistent approvals, or documents that never clearly state what the company is offering.

Use a short control list before any gross-up is promised or paid:

The safest language is plain and specific. Avoid vague references to “covering taxes” unless payroll has already confirmed how that will work.

Here is a simple example for adaptation with legal and payroll review:

The Company will provide a one-time taxable payment in connection with [relocation/bonus/severance]. If approved by the Company in writing as eligible for gross-up treatment, the payment will be processed so that, after applicable withholding based on payroll treatment at the time of payment, the employee is intended to receive the net amount specified in this agreement. The Company reserves the right to determine the calculation methodology and payroll process used to administer the payment.

A narrower version can work better when you want tighter control:

No tax gross-up applies unless this agreement expressly states that the payment is eligible for gross-up treatment.

Three drafting habits create unnecessary exposure:

If your organization is revisiting how it handles gross-ups, relocation support, severance commitments, or multi-state payroll exceptions, a structured policy review can prevent expensive inconsistency later. To talk through a defensible approach, connect with Paradigm International Inc..