A lot of owners reach the same point at the same time. The company is growing, hiring is harder, key roles need stronger bench strength, and someone suggests a tuition reimbursement program as a smart retention move. That is the easy part.

The harder part is building a program that does not create tax problems, uneven manager decisions, payroll disputes, or state law exposure once you operate across more than one jurisdiction. A tuition reimbursement program can be a strong investment, but only if the structure is disciplined from day one.

A supervisor in Texas approves tuition for a medical billing certificate. A manager in Illinois approves an MBA because the employee is a strong performer. A site lead in Arizona denies a similar request because the course does not relate closely enough to the current role. Same company, same benefit, three different standards. That is how a well-intended tuition program turns into an employee relations problem, and in a multi-state business, a compliance problem.

A defensible tuition reimbursement program starts with a narrower question than many owners ask. What business outcome justifies the spend, and what approval standard will hold up when different managers apply it?

For an SMB, tuition reimbursement should solve a workforce problem the company already has. Usually that means reducing turnover in hard-to-replace roles, building promotion paths for key positions, or closing skill gaps that are expensive to hire for on the open market.

The retention case can be strong, but owners should rely on sourced facts, not recycled talking points. Chipotle reported 89% retention after five months for program participants, nearly double the rate for non-participants, as discussed in this retention analysis. That supports the business case for education benefits. It does not justify paying for any course an employee wants to take.

Set the objective before writing the policy. If you skip that step, approvals drift toward personal preference, manager sympathy, and inconsistent exceptions.

A practical framework is to choose one primary objective and one secondary objective:

Once the objective is clear, turn it into criteria that managers can apply without improvising. Good policy design reduces discretion at the point where legal risk usually begins.

That means defining who qualifies, what types of education qualify, when approval must happen, and what evidence the employee must provide. If the answer to those questions changes by department, the program is not ready.

Most defensible programs define:

Tip: If a manager cannot explain the business value of a course in one clear sentence, the job-relatedness rule is too loose.

This is the stage where many SMB programs create exposure. Leadership wants flexibility. Employees hear promises. Managers start making case-by-case decisions that feel fair in the moment and look arbitrary later.

Use a single approval framework across states and departments, then route true exceptions through HR or a designated review committee. That protects the company in two ways. It improves consistency, and it creates a record showing that exceptions were reviewed under a defined standard rather than handed out informally.

A simple decision table helps keep approvals disciplined.

| Approval factor | What a defensible standard looks like |

|---|---|

| Role connection | Supports current duties, a documented advancement path, or a defined business need |

| Employee standing | Meets tenure and performance requirements |

| Program quality | Approved institution or recognized credential |

| Business impact | Builds capability the company expects to use |

| Documentation | Complete application submitted before enrollment |

For employers reviewing the larger benefits structure around this policy, it helps to see how other organizations design an exceptional employee benefits program so tuition assistance aligns with compensation, leave, and career growth policies instead of operating as an isolated perk.

A tuition reimbursement program should be measurable before the first approval goes out. Otherwise, it becomes hard to tell whether the company is funding a talent strategy or just adding cost.

Choose metrics that match the business objective. If the program is meant to support internal mobility, track promotions and backfill rates in covered roles. If the goal is retention, compare participant turnover against a relevant employee group, not the entire company. If the goal is hiring stability, ask whether the program improves acceptance rates or candidate quality in priority positions.

If your benefits strategy is still taking shape, review this guide to small business benefits packages so the education benefit fits a sustainable SMB model instead of becoming a standalone promise with no control structure.

The strongest foundation is clear enough to defend in an audit, consistent enough to survive manager turnover, and narrow enough to produce a return the business can measure.

A tuition reimbursement program fails financially in predictable ways. It is too open-ended, too informal, or too generous up front. In each case, the employer takes on risk before it has proof of completion, proof of value, or confidence that the employee will stay.

That is why SMBs need a more conservative model than the glossy guides suggest.

There are two broad ways to fund education benefits. One is to reimburse after successful completion. The other is to provide some form of upfront support.

The first option is safer for most SMBs. The second can increase access, but it also increases the chance that the company pays for incomplete coursework, loses a negotiating advantage if the employee departs, or creates avoidable administrative disputes.

A clear comparison makes the trade-off easier.

| Model | Main advantage | Main risk |

|---|---|

| Post-course reimbursement | Limits spend until completion is proven | Employees must carry upfront cost |

| Upfront payment or assistance | Reduces employee cash-flow barrier | Employer funds risk before results are known |

For most multi-state employers, risk control matters more than ease of launch. A reimbursement-first structure gives finance, payroll, and HR fewer variables to manage.

A cap is not just a budget number. It is a policy boundary.

The most effective cap is one that leadership can explain and administer consistently. If the number changes by team, manager, or employee popularity, the program starts to look discretionary in the wrong way.

Cost control also improves when the policy answers practical questions up front:

Many owners hesitate to use repayment provisions because they do not want the program to feel punitive. That concern is understandable, but the absence of a clawback can turn a smart benefit into a transfer of value to your next competitor.

According to Bright Horizons, a 2025 Mercer analysis found 40% of program participants leave within 12 months of completing a degree, which is why many firms use pro-rated repayment clawbacks over a 1-2 year period.

That does not mean every departure should trigger repayment. It means the policy should distinguish between legitimate separation scenarios and the voluntary exits the employer is trying to discourage.

A workable clawback framework covers:

Key takeaway: A clawback should be treated like a risk allocation document, not a paragraph added at the end of the policy.

In practice, the biggest cost problems come from exceptions, not from the written policy. A manager wants to approve an unlisted course. Finance agrees to move faster than the normal cycle. HR waives a rule because the employee is high potential.

Each exception may feel reasonable. Collectively, they weaken the program.

A disciplined approval process should require senior review when a request falls outside standard criteria. It should also document why the exception was approved and who authorized it. If exceptions become common, the policy needs revision rather than repeated workarounds.

A tuition reimbursement program earns trust when the economics are predictable. Owners should be able to answer three questions at any time: what the company will fund, when it will fund it, and what protection exists if the employee leaves soon after receiving the benefit.

A business with employees in Texas, California, and New York approves the same tuition request three times. The tax treatment may be consistent. The legal risk is not. That gap is where many small and midsize employers get into trouble.

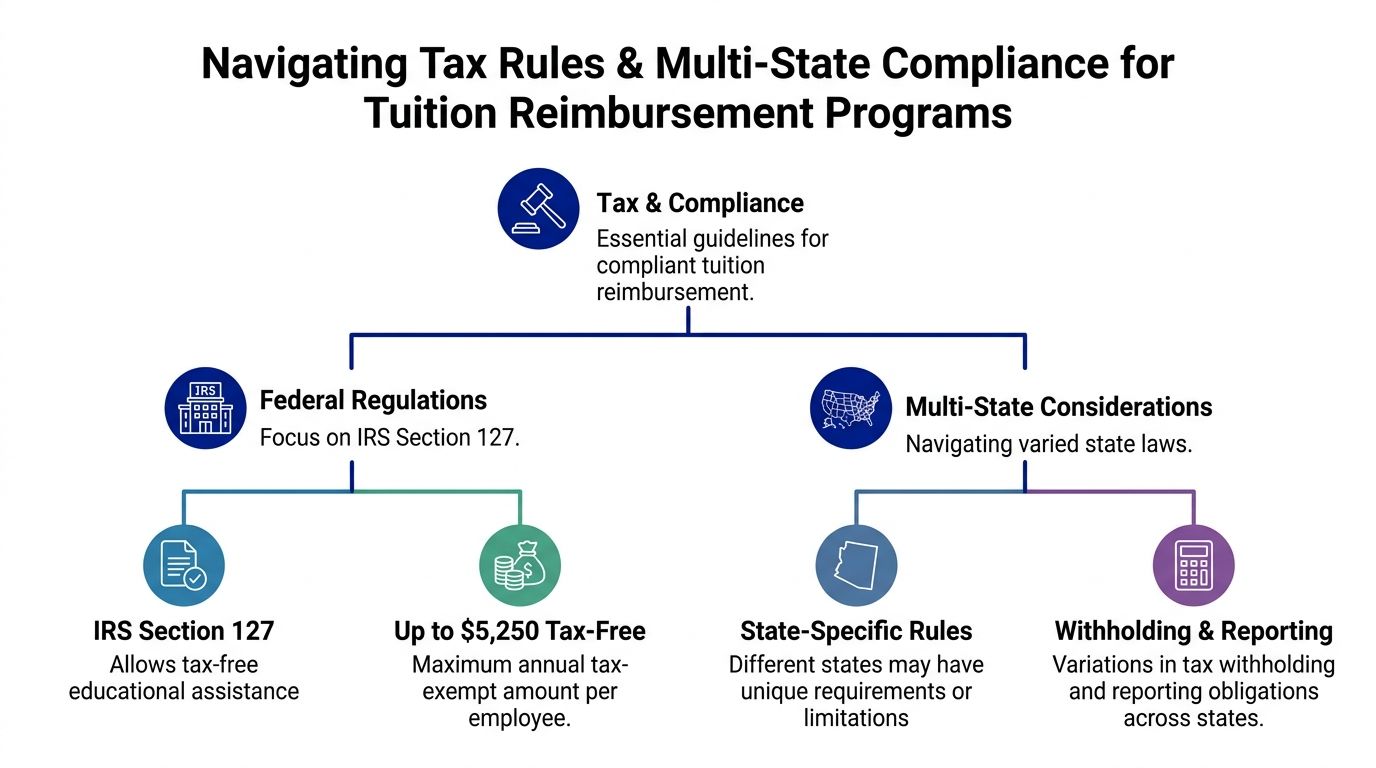

A defensible tuition reimbursement program starts with federal tax law, then gets stress-tested against state wage, payroll, and notice rules. Generic policy templates rarely do that work. If you operate across state lines, that omission can turn a retention benefit into a payroll dispute or a tax reporting problem.

At the federal level, the anchor is IRS Section 127. It allows employers to provide up to $5,250 in tax-free educational assistance per employee each year when the program is set up correctly, as outlined in the IFEBP education benefits survey.

That tax treatment is attractive for a reason. It lets the company fund education without converting the benefit into taxable wages within that annual limit. But the exclusion does not protect a loosely run program. To preserve the tax benefit, employers should define who is eligible, what expenses qualify, and how approvals are made. Informal manager-by-manager arrangements create audit risk and invite inconsistent treatment.

A visual summary helps frame the moving parts:

Federal compliance is only part of the job. State law controls many of the practices that cause disputes in real programs, especially payroll deductions, reimbursement timing, final pay handling, and required disclosures.

Compt’s review of tuition reimbursement compliance issues cites SHRM reporting that multi-state employers commonly run into compliance problems with education benefits because state rules on repayment and administration are not consistent. For an SMB, that is the primary implementation issue. The policy may be lawful on paper and still fail in operation if payroll and HR apply it the same way in every state.

The exposure points are usually operational, not theoretical:

California and New York deserve special attention because they leave less room for casual administration. California is particularly sensitive on wage deductions and pay practices. New York often requires tighter coordination among policy language, payroll process, and employee communications. The exact answer depends on how the program is structured, but the practical rule is simple. Do not assume a process that works in one state will hold up everywhere.

Tip: If the company expects to recover education costs after a resignation, have employment counsel review the collection method before rollout, not after the first dispute.

Separate policies for every state create administrative drag. One generic national policy creates legal blind spots. The better approach is a core national policy with state-specific addenda where needed.

That structure keeps the program recognizable across the company while giving payroll, HR, and counsel room to adjust the parts most likely to create liability.

| Core program element | Best handled nationally or locally |

|---|---|

| Eligibility standards | Nationally |

| Approval workflow | Nationally |

| Documentation requirements | Nationally |

| Tax-favored annual structure | Nationally |

| Wage deduction limits | Locally |

| Required payroll disclosures | Locally |

| Repayment enforcement method | Locally |

This is the same discipline employers need in other multi-jurisdiction employment practices. This review of remote worker compliance across multiple states is a useful reference point for leaders building policies that have to survive different state rules without becoming impossible to administer.

Some employers want to combine tuition reimbursement with student loan repayment support. That can work, but it raises separate tax and payroll design questions, especially when teams assume the same rules apply to both benefits.

For leaders assessing that option, Allied Tax Advisors provides a helpful summary of Student Loan Relief Program Extensions that can inform discussions with tax counsel and payroll providers.

The broader point is risk control. A tuition reimbursement program for a multi-state workforce should be built like an employment policy with tax consequences, not a goodwill perk. Owners who treat it that way usually get the outcome they want: a useful retention benefit, cleaner payroll administration, and fewer surprises when an employee leaves or a state agency starts asking questions.

A manager approves an MBA class for one employee over Slack. Another employee gets denied for a similar request because HR says the coursework is not job-related. Six months later, the first employee resigns, disputes a repayment demand, and payroll cannot show which version of the policy applied. That is how a retention benefit turns into a legal and employee-relations problem.

For a multi-state employer, the documentation process is the control. If the record is incomplete, inconsistent, or split across systems, the company will struggle to justify tax treatment, repayment enforcement, or equal application of the policy.

The file should exist before the employee enrolls or pays anything. Pre-approval creates a defensible decision point and reduces pressure to make exceptions after the fact.

A strong application captures the facts you may need later:

That record matters when two employees request similar support and only one qualifies. It also matters when a state agency, auditor, or plaintiff-side lawyer asks whether the company followed its own rules.

Reimbursement should be released only after the company receives the same categories of proof every time. Informal emails, screenshots without context, and manager-only approvals create avoidable exposure.

A clean reimbursement packet includes:

One practical warning. If HR, payroll, and finance each maintain separate tuition files, exceptions multiply fast. The company needs one complete file and one clear decision trail.

The workflow should survive turnover, vacations, and manager inconsistency. If the process depends on who happens to review the request, the program will drift.

Use a fixed sequence:

Education benefit records should be kept with the same discipline as other employment-related files. If a repayment dispute surfaces or an agency asks how the program is administered, the company should be able to produce a complete record quickly and in the same format for every employee.

That means aligning the benefit file with broader documentation rules instead of treating it as a side process. This guide to employment records retention requirements is a useful reference for setting retention periods, storage ownership, and retrieval practices that hold up under scrutiny.

A tuition reimbursement program is defensible when every approval, exception, reimbursement, and repayment decision leaves a clear paper trail. That is what protects the company when an employee leaves, a tax question surfaces, or two states expect different answers from the same file.

A common failure point for tuition reimbursement programs is the launch itself. An employee enrolls in a course after getting casual approval from a manager, submits expenses late, and then learns the class never met policy requirements. In a multi-state company, that mistake is more than frustrating. It creates inconsistent approvals, repayment disputes, and preventable employee relations risk.

A defensible rollout treats communication as a control, not a courtesy. Employees need to understand how to use the program correctly, and managers need to know where their discretion stops. If either group is guessing, the company will pay for it later through exceptions, appeals, and uneven administration across locations.

Low participation is often blamed on employee disinterest. In practice, many eligible employees either do not know the benefit exists or do not understand how to qualify for it. The problem is worse when the program sits in a handbook, appears once during onboarding, or uses policy language that sounds legal but offers no clear next step.

Launch materials should answer the operational questions employees have:

That last point matters. A multi-state employer should give employees one intake path, usually HR or a designated program owner, rather than letting each manager interpret the rules independently.

Managers shape whether the program is trusted, but they are also a major source of inconsistency. Employees usually ask them first whether a course looks relevant, whether reimbursement is likely, and whether using the benefit will affect performance reviews or promotion chances.

Loose answers create liability.

Manager training should be short, mandatory, and practical. The goal is to prevent off-policy promises and force clean escalation when a request falls outside the standard rules. Leaders do not need a seminar on employee development. They need a script, examples, and a clear boundary between support and approval authority.

A useful manager briefing should cover this:

| Manager responsibility | What good practice looks like |

|---|---|

| Discuss development needs | Connect education requests to role requirements, skill gaps, or approved career paths |

| Avoid verbal approvals | Direct employees to the formal process and avoid saying a course will be covered |

| Apply standards consistently | Use written criteria across teams, offices, and states |

| Record business rationale | Explain how the request relates to the employee's current role or approved progression path |

| Escalate exceptions | Route unusual requests, nontraditional programs, or policy conflicts to HR or legal review |

A safer manager response is simple: “Submit it through the program process, and HR will review it against policy.”

One announcement email will not carry this program. Employees pay attention when they are choosing courses, discussing career growth, or reviewing benefits during open enrollment and performance cycles.

A stronger launch uses several touchpoints over a defined period:

The message should stay concrete. Employees respond to examples such as approved certifications, degree paths tied to internal roles, reimbursement timing, and grade or completion requirements. Broad statements about learning culture do not prevent bad submissions.

Employees judge the program by outcomes, not intent. If one manager waves requests through while another blocks similar courses, the company will lose trust quickly. If one state location applies extra steps that are not written anywhere, the program becomes hard to defend.

That why launch planning and leader training should be tested before full rollout. Use sample cases. Check whether two managers reviewing the same request would give the same answer. Confirm that HR, payroll, and local leaders are using the same terms for approval, reimbursement timing, taxable treatment, and repayment obligations.

A tuition reimbursement program earns confidence when employees can see two things clearly. The company is willing to invest in development, and the rules are applied the same way every time.

A tuition reimbursement program should be reviewed like any other controlled business investment. If leaders only look at annual spend, they miss the signals that matter most.

Useful monitoring starts with a short dashboard, not a giant report. Focus on indicators that show whether the program is aligned, used appropriately, and producing workforce value.

A practical review set includes:

An annual audit should not be a paper exercise. It should test whether the written program still matches how the company runs it.

Review questions should include:

A benefit like this stays low-risk only when someone owns it. That owner does not need to handle every transaction personally, but they do need authority to spot drift, fix weak points, and require consistency across departments.

A tuition reimbursement program can support retention, capability, and internal growth. It can also create unnecessary exposure if it is underwritten loosely. The difference is not intention. It is structure, documentation, and regular review.

If your leadership team is weighing whether to launch, revise, or audit a tuition reimbursement program across multiple states, expert counsel can help you evaluate the policy through a risk, compliance, and defensibility lens so the benefit supports growth without creating avoidable exposure.