A familiar problem lands on an owner's desk this way. A key executive has become essential to the business, competitors are calling, and a standard raise no longer feels like the right answer. More salary increases fixed cost. A cash bonus rewards last year, but it doesn't always protect next year.

That's when leaders start to ask about deferred compensation.

For SMBs, especially those growing across states or relying heavily on a small leadership bench, deferred compensation can be useful. It can help reward a critical person, create a reason to stay, and support longer-term financial planning. It can also create legal, tax, balance-sheet, and communication problems if it's handled casually.

The main mistake I see in executive discussions is treating deferred compensation like a richer bonus plan. It isn't. In practice, it's a future payment promise that has to be designed carefully, documented correctly, and administered with discipline. If your company operates in more than one state, has uneven cash flow, or expects ownership changes in the future, the planning burden rises quickly.

A sound decision starts with the right definition. Not just what deferred compensation means in theory, but what it means for your company, your executives, and the risk you're taking on.

A business owner doesn't usually start by saying, “I need a deferred compensation plan.” The conversation usually starts somewhere more practical. A COO is holding together operations, a physician leader is central to a growing practice, or a sales executive has become hard to replace. The owner wants to reward that person, but also wants a structure that supports retention instead of just increasing annual cash compensation.

That tension is real in SMBs. You need to stay competitive, but you also need to protect cash flow, maintain internal equity, and avoid creating a compensation arrangement you can't administer properly. A larger salary solves one problem and often creates two more. A one-time bonus can feel generous and still do little to keep the person in seat.

Deferred compensation enters the picture because it shifts part of the reward into the future. That changes the conversation from “How much should we pay now?” to “What are we trying to achieve over time?” For the right employee, that can align retention, timing, and long-term planning in a way ordinary cash compensation can't.

Practical rule: If you can't clearly state why the payment needs to happen later instead of now, you're probably not designing deferred compensation. You're probably designing a bonus with extra complexity.

That distinction matters. Once you defer pay, you're dealing with plan terms, distribution timing, possible forfeiture conditions, and a risk profile that many executives don't fully understand at first pass. The company also takes on governance responsibilities that are easy to underestimate.

For SMB leaders, the useful question isn't whether deferred compensation sounds intricate. The useful question is whether the structure fits your actual business condition. If retention is your primary goal, your company's financial stability, legal discipline, and ability to communicate the plan matter as much as the benefit itself.

Deferred compensation is an agreement to pay part of an employee's compensation later, even though the employee earned it through current service.

For an SMB, that timing shift carries real consequences. Once compensation is deferred, the company is no longer deciding only how much to pay. It is also deciding when to pay, under what conditions, and from what future resources. In a single-state business, that already requires discipline. In a multi-state operation, the administrative and legal review usually needs to be tighter because termination rules, wage payment expectations, and document handling can create added exposure.

The core concept is simple. Services are performed now, but payment is scheduled for a later date or event, such as retirement, separation from service, vesting, or another trigger written into the arrangement.

That future payment date is what turns this from a cash compensation issue into a compensation design and risk management issue. If the promise is not documented clearly, funded appropriately for the company's condition, and explained accurately to the employee, the plan can create misunderstandings that are expensive to fix.

Employers usually adopt deferred compensation to solve a specific business problem, not to add another benefit for its own sake.

The trade-off is straightforward. Deferred compensation can improve retention and timing, but it also creates a future liability. If the business hits a downturn, changes ownership, or faces a liquidity crunch, that promise can become harder to honor at the exact moment the employee is counting on it.

A good deferred compensation arrangement answers three questions clearly: why payment is delayed, what event triggers payment, and how confident the company is that it can pay when the obligation comes due.

Deferred compensation is not just any payment made later. If a company pays a bonus late because of payroll timing or internal delay, that is not the same thing as a structured deferral arrangement. A true deferred compensation plan sets the terms in advance.

It also should not be described carelessly as guaranteed or fully protected unless that is true under the plan structure. That is where SMB leaders get into trouble. Employees may hear “retirement benefit” and assume the money is segregated, protected from creditors, or treated like a standard qualified plan. In many arrangements, that assumption is wrong.

From a risk advisory standpoint, the definition matters because labels drive expectations. If the company treats deferred compensation as a loose side agreement, HR inherits communication problems, finance inherits an unmanaged liability, and leadership inherits legal risk that could have been avoided with a tighter framework.

A 25-person company with operations in Texas and California usually does not ask for "deferred compensation" in the abstract. It asks a narrower question: do we need a broad retirement benefit, or are we trying to keep two or three people through a financing round, ownership transition, or succession plan? That distinction determines the plan category, the compliance burden, and the balance-sheet risk you are taking on.

In practice, deferred compensation usually falls into two buckets: qualified plans and nonqualified plans. SMB leaders should treat them as different tools for different problems, not interchangeable benefit labels.

Qualified plans include familiar arrangements such as 401(k), 403(b), and 457(b) plans. These plans are built for a wider employee group and sit inside a more standardized regulatory framework.

For most SMBs, that means qualified plans are the workforce tool. They support hiring, create a recognizable retirement benefit, and are generally easier to explain during onboarding and annual enrollment. Finance and HR also tend to have clearer processes around them because vendors, payroll teams, and employees already recognize the structure.

The trade-off is flexibility. Qualified plans are usually not the best choice when leadership wants to retain one revenue-producing executive or create a special payout schedule for a founder-level operator who plans to exit in three years. They are stronger for consistency than for select-person retention design.

Nonqualified deferred compensation plans, or NQDC, are more often used for executives and highly compensated employees. They can permit higher deferrals and more discretion around payout timing, which is why owners often consider them during succession planning, sale preparation, or long-term retention discussions.

That design freedom is useful, but it raises the stakes. A business can set terms that fit a specific retention objective, then discover later that the documentation, election timing, or payout triggers were not handled with enough precision. In a multistate business, that problem can spread beyond tax timing into wage payment, termination, and claims-handling issues if the plan language and employment agreements do not line up.

Funding risk is usually the point executives underestimate. In many NQDC arrangements, the promised amounts are still part of the employer's general assets and may be exposed to creditor claims. So the retention value is real, but so is the solvency question. If the company cannot comfortably carry the future obligation, the plan can create more risk than loyalty.

For a more practical breakdown of how these arrangements work, see this overview of a non-qualified deferred compensation plan structure.

| Plan category | Typical fit | Main strength | Main caution |

|---|---|---|---|

| Qualified | Broad employee groups | Familiar retirement structure and tax-advantaged savings | Less suited to selective executive retention |

| Nonqualified | Select executives or highly compensated employees | Greater flexibility in deferral and payout design | Often tied to employer general assets and added compliance risk |

Use the qualified route when the business goal is broad coverage, predictability, and a benefit employees can understand quickly. Consider NQDC when the goal is narrower and more strategic, such as retaining a key operator, phasing out an owner, or rewarding a small leadership group without extending the same design to everyone else.

The mistake I see most often is choosing the more flexible option before testing whether the company can administer it cleanly and pay it under stress. A deferred compensation plan is not just a retention promise. It is a future obligation that has to survive turnover, disputes, and uneven cash flow.

A common SMB scenario looks like this. The owner wants to retain a key executive, the executive likes the tax deferral, and everyone agrees on the concept before anyone has tested the company's ability to fund the promise through a bad year, a leadership change, or an acquisition. That is where deferred compensation starts to shift from a benefit discussion to a risk decision.

The tax treatment is simple at a high level. Deferred compensation is generally taxed when the employee receives it rather than when the employee earns it, as summarized in Wikipedia's deferred compensation overview. That timing can help an executive manage taxable income across years.

The tax angle gets attention because it is easy to explain. It is rarely the hardest part of the decision.

For the employer, the harder questions are operational and financial. Can the business carry the obligation on its books without stressing future cash flow? Can payroll, finance, and HR administer elections and payout timing correctly? Can leadership explain the plan clearly enough that participants understand they may be depending on the employer's future solvency, not on a protected account set aside for them?

Employees often view deferred compensation as part retirement planning and part tax planning. That is reasonable. Owners and HR leaders should still keep the message disciplined. If the plan is sold mainly on tax savings, participants may overlook liquidity limits, forfeiture terms, and the restrictions around changing elections after the fact.

That is where bad expectations start.

For owners who want broader context on tax strategy beyond deferred compensation, this resource on effective tax planning for businesses is a helpful companion to the compensation discussion.

Leaders comparing deferred compensation with other salary reduction concepts should also separate these ideas carefully. A pre-tax contribution structure does not carry the same legal and funding issues as a nonqualified deferred compensation promise.

Many nonqualified deferred compensation arrangements are unsecured obligations of the employer. In practice, that means the employee is an unsecured creditor until payment is made. If the company runs into distress, the participant may have a contractual claim without having assets isolated for that person's benefit.

That point matters more in SMBs than many leaders expect.

A mature company with steady margins and disciplined reserves can sometimes support a narrow deferred compensation program without straining the business. A company with uneven revenue, high debt, pending expansion, or owner-distribution pressure should pause and model the downside first. A plan that feels affordable in a strong year can become a real burden during a downturn, partner dispute, refinancing, or sale process.

I usually tell leadership teams to answer one question in plain language before they offer the plan: if two participants separate in the same quarter and both distributions come due, where does the cash come from?

If the answer is vague, the plan is not ready.

Section 409A is one of the main compliance rules governing nonqualified deferred compensation. For SMBs, the practical lesson is straightforward. Timing rules for elections and distributions need to be set correctly at the start and followed closely after that.

When the plan is drafted loosely or administered casually, the participant can face immediate taxation, an extra 20% federal tax, and interest penalties. Those consequences are serious enough that hand-built processes, side agreements, and informal exceptions are dangerous. The document, the election process, the payroll treatment, and the payout event definitions all need to match.

This is one reason multi-state employers need tighter internal coordination. The federal rule may control the tax framework, but state payroll practices, employment agreements, separation handling, and record retention can still create friction if teams are not working from the same definitions.

The risk picture gets more complicated once a company operates across state lines. Different HR teams may use different separation practices. Payroll may sit in one state, legal counsel in another, and executive agreements may have been drafted at different stages of growth. That is how administration starts to drift.

Before approving or expanding a deferred compensation plan, review these points:

Well-run deferred compensation plans can support retention and reward a small leadership group effectively. Poorly run plans create a future payment obligation, a tax compliance problem, and a trust problem at the same time.

A founder in Texas promises a future payout to keep a COO through a three-year expansion. Six months later, the company adds operations in California and New York, changes payroll providers, and hires a new controller. The retention goal still makes sense. The administrative risk is now much higher.

That is how deferred compensation shows up in real companies. The plan design is not just a reward mechanism. It is a business commitment that has to survive growth, leadership changes, and uneven state-by-state HR practices.

In practice, SMBs usually use deferred compensation for one of three reasons: retain a key operator, push performance beyond the current bonus cycle, or give a senior executive additional retirement-timing flexibility. The right structure depends on the problem being solved, the company's cash tolerance, and how much administrative discipline leadership is willing to maintain over time.

A multi-state company may depend heavily on one COO to standardize hiring, stabilize service delivery, and keep expansion from becoming operational drift. In that case, a deferred compensation promise can help keep that person in place through a defined period.

A common design is a future payment tied to continued service through a specific date, retirement, or another permitted payment event. The benefit is straightforward. It gives the executive a reason to stay without permanently increasing fixed cash compensation.

The trade-off is equally straightforward. If the company is using deferred compensation to cover up current frustration over authority, staffing, ownership, or burnout, the plan will not solve the underlying problem. It may just postpone an expensive departure.

For multi-state employers, this scenario also needs clean execution across entities, payroll, and separation documentation. A retention design can break down quickly if one team records a departure as a resignation, another treats it as an involuntary termination, and the plan language does not line up with either one.

Some companies want to reduce the short-term bias built into annual incentive plans. A sales leader may hit quota every year, but leadership wants stronger account retention, cleaner renewals, and less revenue that disappears after the payout is made.

A deferred bonus arrangement can work well here. Part of the earned incentive is scheduled for later payment, usually subject to continued service and clearly defined conditions. That structure shifts attention from booking revenue fast to protecting value over a longer period.

This design requires discipline in plan drafting and participant communication.

If the company describes the award casually as money that is already "set aside," expectations can drift away from the legal and financial reality. That misunderstanding creates trouble later, especially if business conditions weaken or the employee leaves before the payment date.

Good deferred compensation design rewards behavior the company wants repeated and does not create promises the company may struggle to explain or fund later.

A long-tenured executive may have already used the usual retirement plan options and want more control over when compensation is received. The company may also want to recognize that person's contribution without changing benefits for the broader workforce.

In that situation, a selective deferred compensation arrangement can provide scheduled future income tied to retirement or another valid distribution event. For the executive, the appeal is timing. For the employer, the appeal is targeted reward rather than broad plan expansion.

The risk sits in the long tail. Retirement-focused arrangements often look manageable at signing because the payment date feels distant. Years later, the company may have different ownership, tighter cash flow, or a weaker balance sheet than anyone expected when the promise was made.

That is why I tell SMB leaders to test this scenario against a bad year, not a good one. If the payout would feel painful during a downturn, the design needs revision before it goes on paper.

The business purpose changes from case to case, but the operating questions stay fairly consistent:

A workable design is one the company can explain clearly, administer consistently, and afford under stress. If it fails one of those tests, it is not ready yet.

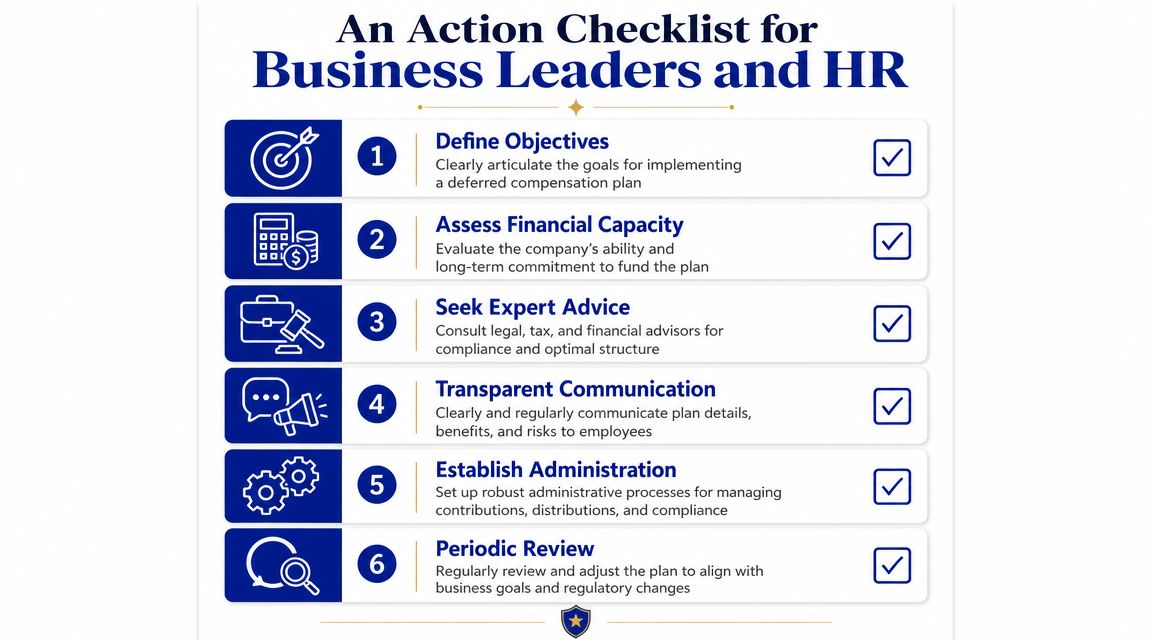

Before a company offers deferred compensation, leadership should pressure-test the decision from multiple angles. This is not just a benefits decision. It's a compensation, governance, finance, and risk decision.

A plan should begin with a specific objective.

At this stage, many plans should slow down.

A deferred compensation promise is easy to approve in a good year. The real test is whether the company will still want, and be able, to honor it later.

A plan should never go live before the legal and administrative pieces are settled.

If you're evaluating outside support for the broader compensation architecture around executive pay, a compensation consultant can help frame the decision before documents are drafted.

This part is often underdone. Executives need a clear explanation of what they are receiving, when they may receive it, and what risks remain attached to the promise.

Use plain language. Explain whether the arrangement is unsecured. Explain what continued employment requirements apply. Explain what happens if the company changes ownership, if the executive separates, or if administration errors occur.

A short communication checklist helps:

Once implemented, deferred compensation needs periodic review. Business conditions change. Leadership changes. State footprint changes. Plan administration can drift.

At a minimum, leadership should revisit whether the plan still serves its original purpose, whether records are complete, and whether the company still has the financial and administrative capability to carry it responsibly.

If your leadership team is weighing deferred compensation and wants a practical risk review before moving forward, Paradigm International Inc. can help you assess the decision, pressure-test the structure, and support a more defensible approach for a growing business.