Yes, companies do pay for unemployment. In most cases, they pay through employer unemployment taxes, including a federal tax of 6.0% on the first $7,000 of each employee's wages, often reduced to an effective 0.6%, which means the federal portion is typically up to $42 per employee per year.

If you're looking at an unemployment claim notice and wondering whether your business is about to get billed directly for a former employee's benefits, the answer is usually no. The employee isn't paid by a check from your company. But that doesn't mean the claim is free. Unemployment is one of those costs that looks passive on the surface and turns into an operational issue once claims, documentation, and state experience ratings come into play.

That's the part many leaders miss. The question isn't just, “Do companies pay for unemployment?” It's whether the organization is managing that cost deliberately, or letting weak documentation, inconsistent terminations, and avoidable claim approvals drive it upward over time.

The usual moment this becomes real is when a state notice lands in payroll, HR, or your inbox. A former employee has filed for unemployment, and someone on the leadership team asks whether the company now owes that person money.

The short answer is still yes, companies pay for unemployment, but they usually pay into a system rather than paying the former employee directly. In the United States, unemployment insurance is generally funded through employer payroll taxes. Under FUTA, employers pay tax on the first $7,000 of each employee's wages at a standard 6.0% rate, which is often reduced to 0.6% if the employer receives the full federal credit by staying current on state taxes. That makes the maximum federal unemployment tax typically $42 per employee per year, and only a few states, Alaska, New Jersey, and Pennsylvania, also require employee contributions, as explained in Oyster's overview of who pays for unemployment.

Think of unemployment insurance like a pooled insurance structure.

You fund it in two layers:

That's why the phrase “the government pays unemployment” is only partly true. State agencies administer benefits, but employers finance the system that makes those payments possible.

Practical rule: Treat unemployment taxes as part of labor cost, not as a background compliance line item.

The federal portion is usually not what catches leaders off guard. The bigger issue is that state unemployment obligations behave more like an insurance premium tied to your workforce history than a fixed administrative fee.

For operating leaders who already monitor labor cost tightly, this belongs in the same conversation as staffing models and payroll controls. If you're already working on managing restaurant COGS and payroll, unemployment should sit beside those metrics because it reflects staffing decisions, turnover, and claim handling discipline.

A lot of confusion also comes from terminology. Teams hear FUTA, SUTA, reserve accounts, chargebacks, and tax rates, but they don't always understand how those pieces fit together. A good starting point is a practical explanation of SUI tax and what employers should know, because once you understand the funding structure, the later claim notices make more sense.

Most employers spend too much time looking at the federal tax line and not enough time looking at what moves their cost. The federal side is predictable. The state side usually isn't.

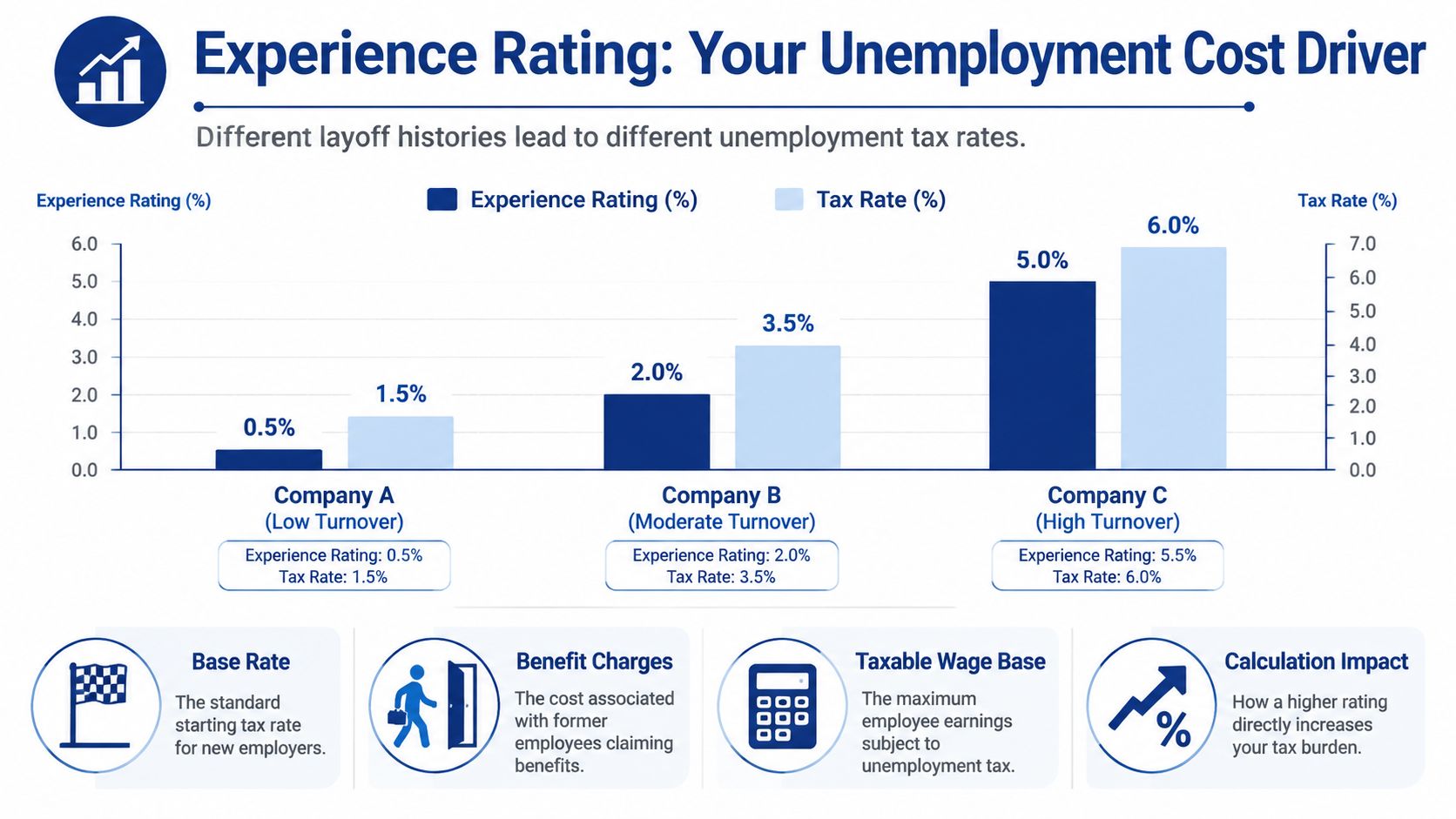

The bigger liability is often driven by experience rating, which is why two employers in the same state can face very different unemployment costs. ADP explains that the federal FUTA rate is 6% on the first $7,000 of each employee's annual wages, with a potential 5.4% credit that can reduce the effective rate to 0.6%. That keeps the maximum recurring federal employer cost typically at $42 per employee per year, but the more important issue is that states often adjust SUTA rates upward when a firm has more successful claims, as outlined in ADP's explanation of who pays for unemployment.

A useful analogy is auto coverage. A driver with a clean record usually pays less than a driver with repeated claims. State unemployment systems work in a similar way.

If your organization has more approved unemployment claims, your SUTA rate can rise. If your workforce practices lead to fewer chargeable claims, your rate can be more favorable. That's why unemployment shouldn't be treated as a passive compliance expense. It's a business outcome tied to how the company hires, manages, documents, and separates employees.

A CEO doesn't need to calculate the state formula by hand. But leadership should understand what tends to influence the result.

Here's what generally matters most:

| Business pattern | Likely effect on unemployment cost |

|---|---|

| Stable workforce and clear records | More controllable SUTA exposure |

| Frequent turnover with weak documentation | Higher risk of adverse rate impact |

| Consistent claim response process | Better chance of protecting the employer record |

A rising unemployment rate from the state is often an HR signal before it's a finance problem.

That's the strategic point. Experience rating turns people management into a measurable cost driver. If terminations are rushed, if performance records are thin, or if managers say one thing in meetings and document another, the tax system eventually reflects it.

Once a former employee files for unemployment, the state usually sends a notice to the employer asking for facts about the separation. That notice matters more than many organizations realize. It's where your records, timelines, and internal consistency start getting tested.

A key feature of unemployment insurance is that employer accounts can be charged when former employees claim benefits. Benefit charges are often allocated back to prior employers based on wages paid during the worker's base period. Michigan's fact sheet gives a clear example: if the separation was not disqualifying, the most recent employer can be charged for the first two weeks of benefits, and the remaining charges are then spread proportionately across base-period employers, as described by the Michigan Unemployment Insurance Agency's explanation of employer benefit charges.

A disciplined employer process usually looks like this:

The strongest responses are usually boring. They are consistent, well-dated, and backed by records created before the claim was filed.

Weak responses tend to follow a familiar pattern:

The appeal usually turns on what the employer can prove, not what the employer believes.

If you appeal, keep the same discipline. Use dates, policies, witness knowledge, and documentation. Don't broaden the story on appeal in a way that conflicts with what the company already told the employee or the state.

A CEO approves a remote hire in Colorado for a team managed from Texas, paid through a headquarters payroll team in Illinois. Six months later, the employee separates and files for unemployment. The first question is simple but expensive if your records are sloppy: which state owns the claim, and was the company set up there correctly in the first place?

That is where unemployment stops looking like a routine tax line and starts acting like an operating control problem. Multi-state employers do not just face different rates. They face different registration rules, wage bases, claim procedures, and fact patterns tied to where the employee performed the work.

The U.S. Department of Labor explains that unemployment insurance is a joint federal-state program administered by the states under federal guidelines. In practice, that means remote work can shift liability, reporting, and claims handling away from the state your leadership team thinks of as the company's home base.

The risk usually shows up through ordinary management failures, not exotic legal issues.

A remote employee relocates and nobody updates the work state in payroll. A business hires in a new state before registering for unemployment there. A manager documents attendance problems one way in the office and a different way for remote staff. At separation, HR is left trying to defend a claim with records built under the wrong state setup or inconsistent standards.

Those mistakes carry two costs. One is compliance cleanup, including back registration, tax corrections, and internal time. The other is long-tail cost through claims that are harder to contest and experience rating that can worsen later.

Common pressure points include:

This is why remote growth often raises unemployment cost even when headcount planning looks disciplined. The tax follows operations. If operations are loose, the unemployment file usually shows it.

Single-state habits rarely hold up once employees are spread across several jurisdictions. Companies need one owner for unemployment administration, but they also need clean inputs from payroll, HR, managers, and anyone approving remote work arrangements.

The practical fix is control at the front end. Confirm the employee's primary work state before hire. Require notice and review before any relocation. Route every unemployment notice to one accountable team. Use separation templates that stay consistent on the facts while allowing state-specific handling where needed.

A workable framework usually includes:

For companies expanding distributed teams, remote worker compliance across multiple states is the larger operating issue around this problem. Unemployment is often where weak location controls, inconsistent documentation, and poorly managed separations first turn into measurable cost.

A claim lands on Friday afternoon. HR pulls the file and finds scattered notes, a vague termination email, and a manager who described the separation three different ways. At that point, unemployment cost is no longer a tax issue. It is an operations issue, and the record usually decides how expensive it becomes.

Effective cost control starts long before a former employee files. Employers that keep unemployment costs in check usually do three things well: they document expectations early, execute separations with discipline, and respond to claims with facts that hold together under review.

A defensible claim response begins with ordinary management habits.

The basics are straightforward:

The common failure point is simple. The manager has been frustrated for months, but the file shows little beyond informal complaints. Once a claim is filed, the company tries to assemble a clean story from memory, and that usually produces gaps, contradictions, or language that weakens the case.

Field insight: If the first serious documentation appears on the day of termination, the employer has usually waited too long.

Terminations create concentrated unemployment exposure because the separation reason becomes the center of the claim file. Precision matters more than volume. A short, consistent record beats a long file filled with mixed messages.

A stronger termination process usually includes:

If your team is tightening separation practices, this guide to the employee exit process and related risk controls is a useful place to start.

CEOs often treat unemployment as an HR administration issue. In practice, front-line managers create much of the evidence that later supports or undermines the company's position.

Training should cover what creates avoidable risk:

Managers also need a simple standard for what good looks like:

Unemployment therefore becomes a management-quality metric. Weak supervision, inconsistent write-ups, and casual termination language often show up later as higher claim costs.

A blanket contest strategy usually wastes time and hurts credibility. Some claims should be accepted because the separation does not support disqualification. Others deserve a full response because the file is strong and the facts are clear.

A practical standard looks like this:

| Claim situation | Better employer response |

|---|---|

| Well-documented misconduct or clear voluntary quit | Respond fully and consider protest or appeal |

| Layoff or non-disqualifying separation | Provide accurate facts without forcing a weak contest |

| Incomplete file or contradictory manager record | Fix the internal process first and assess the claim realistically |

The organizations that control unemployment costs best are usually the ones with cleaner files and tighter manager discipline. They answer on time, choose their contests carefully, and treat each claim as feedback on how well the business is managing people before separation ever occurs.

If you've ever asked, “Do companies pay for unemployment?” the useful answer is bigger than yes. Companies fund the system through employer taxes, and their actual cost exposure depends heavily on how well they manage the employment relationship before and after separation.

That reframes unemployment completely. It's not just a tax line. It's a practical indicator of HR control quality. When unemployment costs start rising, leadership should look beyond finance and ask harder questions about turnover patterns, manager consistency, documentation standards, and termination discipline.

The most effective organizations treat unemployment as an operational metric. They don't wait for claims to reveal process gaps. They build cleaner records, train managers earlier, route notices quickly, and make fact-based decisions about when to contest and when to accept a claim.

For businesses operating across states or in regulated environments, the risks are greater because one weak process can multiply across locations. A more defensible HR framework won't eliminate every claim, but it can help reduce preventable exposure and make the unavoidable claims easier to manage.

If your leadership team wants to strengthen the way it handles terminations, documentation, and multi-state employment risk, you can contact the team at Paradigm to learn more.

If your organization is dealing with unemployment claims, inconsistent documentation, or growing multi-state complexity, Paradigm International Inc. works with leadership teams to build defensible HR practices around high-risk people decisions. Their advisory approach is designed for companies that need structure, judgment, and stronger operational control as they grow.