If you're reviewing benefits elections, updating payroll deductions, or answering an employee who wants to “max out” an HSA, the hard part usually isn't the headline number. It's making sure the number is right for that person, that employer funding is counted correctly, and that a mid-year plan change doesn't create an excess contribution problem later.

That's why HR teams and business owners need a more operational answer to how much you can put into an HSA. The IRS gives a clear annual limit, but actual administration depends on coverage type, age, eligibility timing, and contribution coordination across payroll and the HSA custodian.

A common year-end problem starts with a simple payroll question. An employee elects the full HSA maximum during open enrollment, the company also schedules employer contributions, and no one notices the combined total until excess dollars have already gone to the custodian.

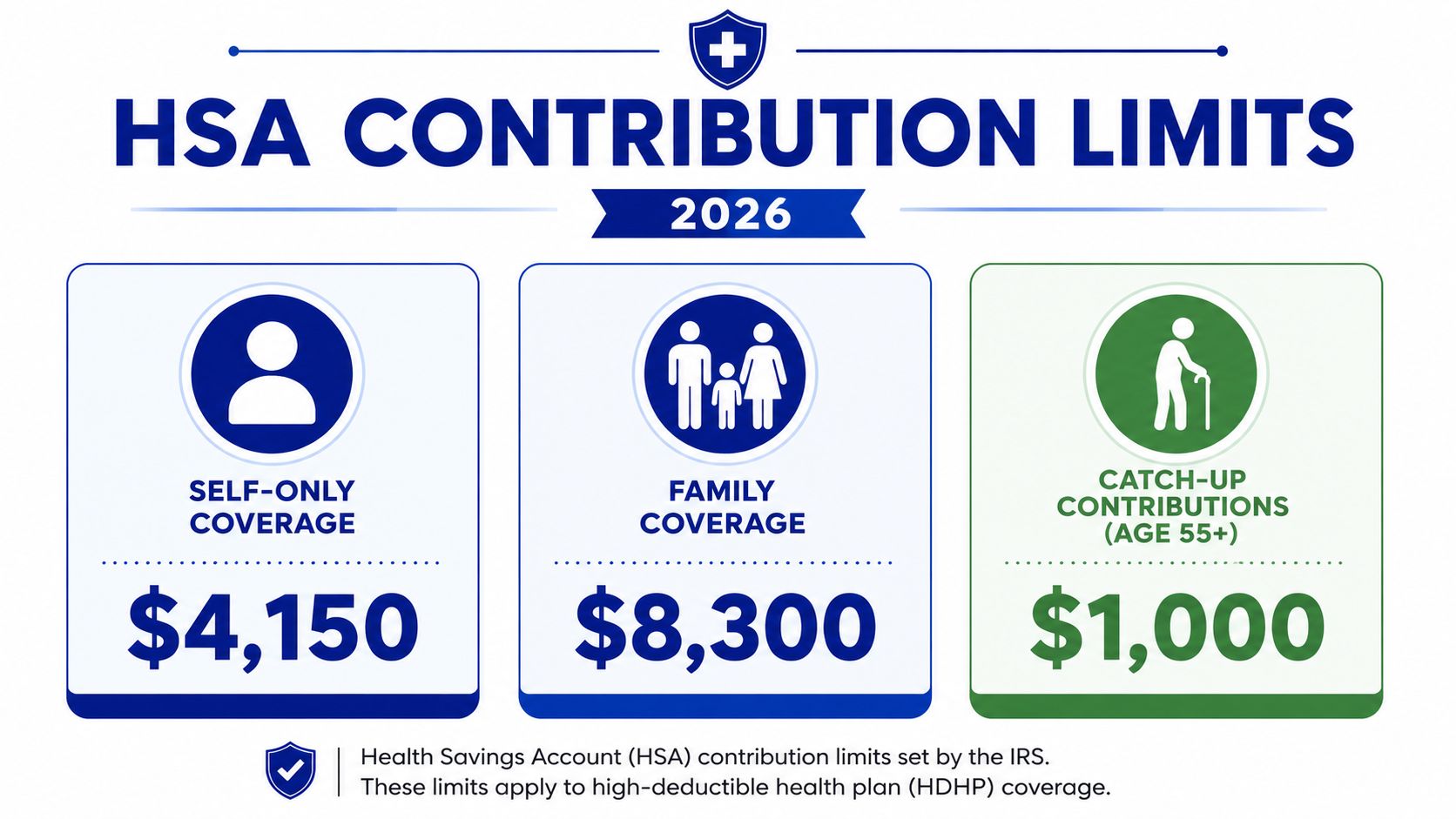

For calendar year 2026, the HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage. Those limits are annual caps on total HSA funding for an eligible individual, not separate buckets for the employee and the employer.

From an administration standpoint, the first question is the employee's coverage tier.

| Coverage type | 2026 annual limit |

|---|---|

| Self-only coverage | $4,400 |

| Family coverage | $8,750 |

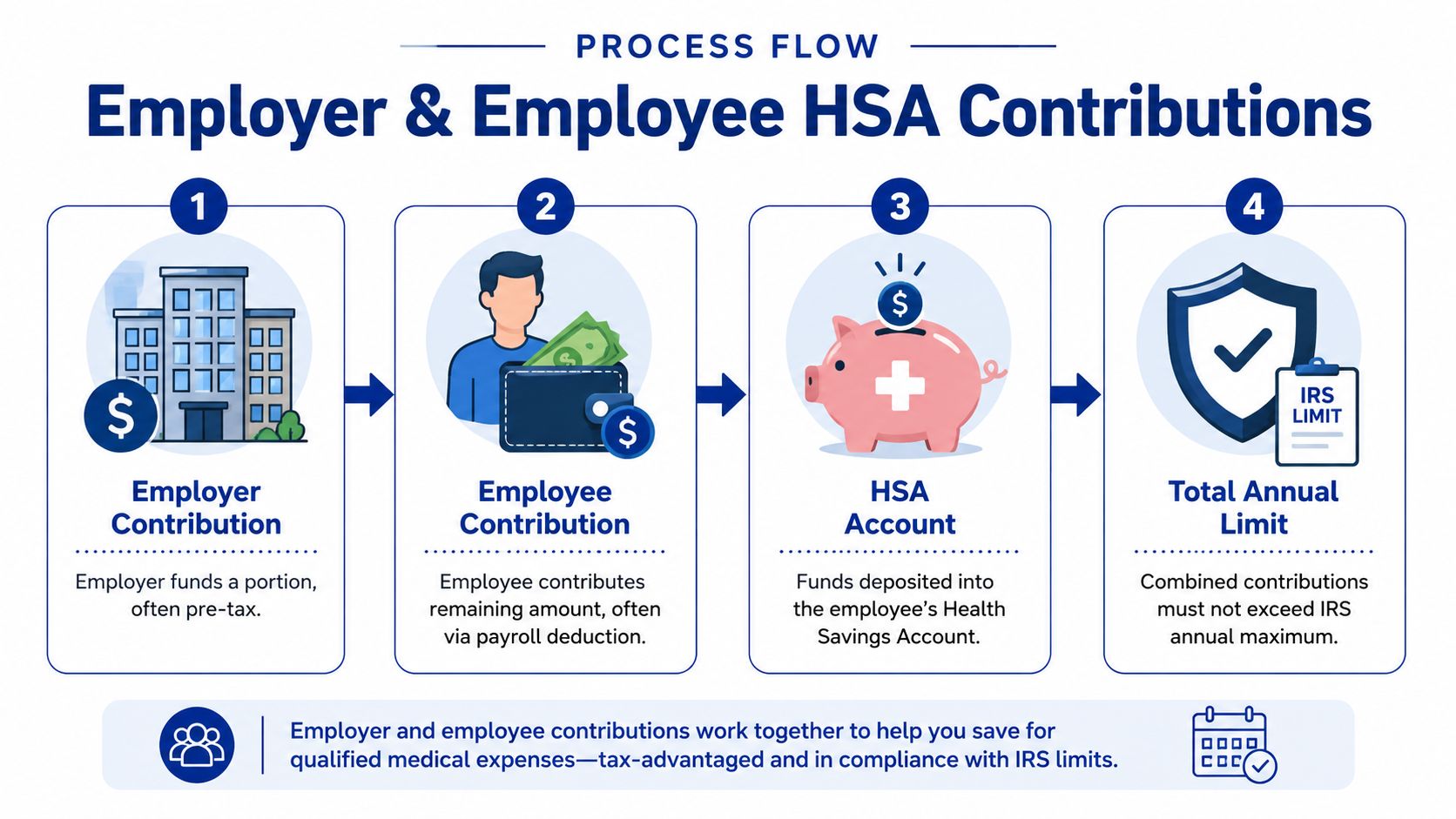

That sounds straightforward, but HR teams have to apply the limit to the full amount contributed to the HSA for the year. Employer seed funding, matching contributions, wellness incentives deposited to the HSA, and employee salary-reduction elections all count toward the same annual cap.

If an employee asks to contribute the full annual amount through payroll, the correct answer depends on what the employer has already committed to fund. A $500 employer contribution reduces the employee's remaining room under the annual limit by $500. If payroll ignores that offset, the excess usually has to be corrected after deposit, which creates extra work for HR, payroll, and the employee.

Annual limits change, and older settings often stay in place longer than they should. For 2026, the IRS increased the limit from the prior year for both self-only and family coverage. That means open enrollment materials, payroll deduction defaults, and any employer funding schedule should be reviewed before the new plan year starts.

This matters more in smaller organizations because HSA administration is rarely housed in one system. Benefits elections may sit in the enrollment platform. Pre-tax deductions run through payroll. The account balance and posted contributions sit with the HSA trustee or custodian. If one record reflects the wrong annual maximum, the mistake may not surface until after multiple pay cycles have run.

The practical control is simple. Confirm the employee's coverage category, confirm every employer dollar scheduled to go into the HSA, and set payroll deductions against the remaining annual limit. That approach prevents avoidable excess contributions and gives HR a clean record if questions come up later.

A common year-end problem starts like this. Payroll has an employee on family HDHP coverage who turns 55, increases HSA deductions, and assumes the extra room works the same way for the household as it does for the employee. That is where overfunding and cleanup work begin.

The age 55+ catch-up contribution adds $1,000 above the regular annual HSA limit. It applies to the eligible person, not to the family contract or the employer's coverage tier. For HR and payroll teams, that distinction matters because the catch-up rule often breaks standard deduction logic that was built only around self-only versus family coverage.

An employee who is age 55 or older may contribute the extra amount if the employee is otherwise HSA-eligible. A spouse who is age 55 or older may have a separate catch-up opportunity, but that amount is tied to the spouse's own eligibility and HSA.

For administration, use these rules:

That third point causes real confusion in small businesses. On family coverage, HR teams often assume one account can absorb the full household amount. It usually cannot. If both spouses want to make catch-up contributions, each spouse generally needs an HSA in that spouse's own name for that extra amount.

The rule is short. The setup work is not.

Many payroll systems have one annual HSA field and one employee deduction election. That works for standard contributions. It does not always work cleanly once an employee turns 55 mid-year, changes elections after open enrollment, or asks HR whether a spouse's catch-up can run through the company plan. A benefits team that does not document those facts can apply the extra $1,000 to the wrong person or allow payroll to exceed what the employee can contribute through that account.

A safer process is to verify four items before changing deductions: the employee's age, current HSA eligibility, whether the catch-up is for the employee or the spouse, and whether the receiving HSA is titled correctly. Teams reviewing pre-tax contribution rules and payroll treatment should treat the catch-up as a separate compliance check, not just an increase to the normal election amount.

For employers trying to keep health benefits and retirement administration aligned, it also helps to discover small business health and retirement plans that fit the company's actual administrative capacity.

A short written enrollment note can prevent a long correction cycle later. State clearly that the age 55+ catch-up is individual, that spouse catch-up amounts usually require the spouse's own HSA, and that payroll changes should be requested promptly when age or eligibility changes occur.

Most HSA mistakes don't start with the IRS limit. They start with fragmented administration.

An employee elects a payroll deduction. The company adds a contribution. Someone also makes a direct deposit into the HSA outside payroll. By the time questions surface, several parties have funded the same account and nobody has a complete year-to-date picture.

The core administrative rule is that employer and employee contributions share one annual ceiling. That sounds obvious, but in practice, many teams still operate as if the company contribution is separate from the employee election.

A defensible process usually includes these controls:

Businesses evaluating broader benefit funding strategy often compare HSA design with retirement and medical plan structure at the same time. If you're reviewing options, this overview to discover small business health and retirement plans can help frame how those decisions connect.

Pre-tax payroll deductions are the cleanest path because the employer can monitor them in the same system that handles compensation. But they aren't the only path.

Employees may also make direct HSA contributions outside payroll. When that happens, the company may have no real-time visibility into the total annual amount. That's why employee communication matters just as much as system controls.

A strong practice is to pair HSA enrollment materials with a short explanation of pre-tax contribution mechanics so employees understand the difference between payroll-based funding and money they deposit on their own.

Administrative test: If an employee asked for their total HSA funding through today, could payroll and HR answer confidently without reconciling three separate systems?

If the answer is no, the process needs work. The risk isn't theoretical. Excess contributions can trigger tax issues, correction work, and avoidable frustration for the employee.

Open enrollment is closed, payroll is set, and then a new hire starts in August and asks to max out their HSA by year-end. That request is common. It is also where HR teams and small employers get into trouble if no one checks monthly eligibility, coverage tier changes, and whether the employee plans to rely on the last-month rule.

The annual HSA maximum is only available to someone who was eligible for the full year, unless a special rule applies. In practice, that means HR cannot treat every employee election as a simple annual limit divided by remaining pay periods.

The pressure points are predictable. New hires enroll mid-year. Employees move from self-only to family coverage or the reverse. Some waive the HDHP during the year, enroll in other disqualifying coverage, or stop being eligible for reasons payroll does not see automatically.

For SMBs, the control question is simple. On the first day of each month, was the employee HSA-eligible, and what coverage tier applied?

That answer drives proration. If payroll keeps taking the same deduction after a status change, the overcontribution usually starts before anyone notices. Employers comparing funding approaches across medical and tax-advantaged benefits should build these controls into their broader small business benefits package strategy, not treat HSA administration as a stand-alone payroll setting.

An employee who is HSA-eligible on December 1 may be able to contribute up to the full annual limit instead of a prorated amount. The rule can help late-year hires, but HR should treat it as an exception that requires explanation and documentation, not as an automatic courtesy.

The catch is the testing period. If the employee does not remain eligible through December 31 of the following year, the extra amount contributed under that rule can become taxable income, and an additional tax may apply. IRS guidance discusses that result in Publication 969.

I advise clients to slow this down for one reason. The employee often hears, "You can make the full contribution," and misses the condition attached to it.

A workable review process includes:

This is not just a calculation issue. It is a communication issue between HR, payroll, the HSA custodian, and the employee.

For example, an employee who changes medical elections in the fall may also be planning other HSA spending decisions, including purchases they believe qualify, such as running shoes that accept HSA. If the contribution side is wrong, the employee may assume the account balance is available and properly funded when it is not.

That is why good administration requires two things at the same time. Accurate proration in payroll, and clear notice to the employee about what changed, when it changed, and whether any deduction adjustment is still needed before year-end.

For SMBs, that discipline matters. Mid-year HSA errors rarely start with a complex tax question. They usually start with an ordinary status change that no one translated into a contribution update.

A common HSA compliance problem starts after open enrollment, not during it. HR approves an employee election, payroll starts deductions, and only later does someone notice the employee had disqualifying coverage or state tax treatment that works differently from federal treatment. By then, the company is dealing with corrections instead of clean administration.

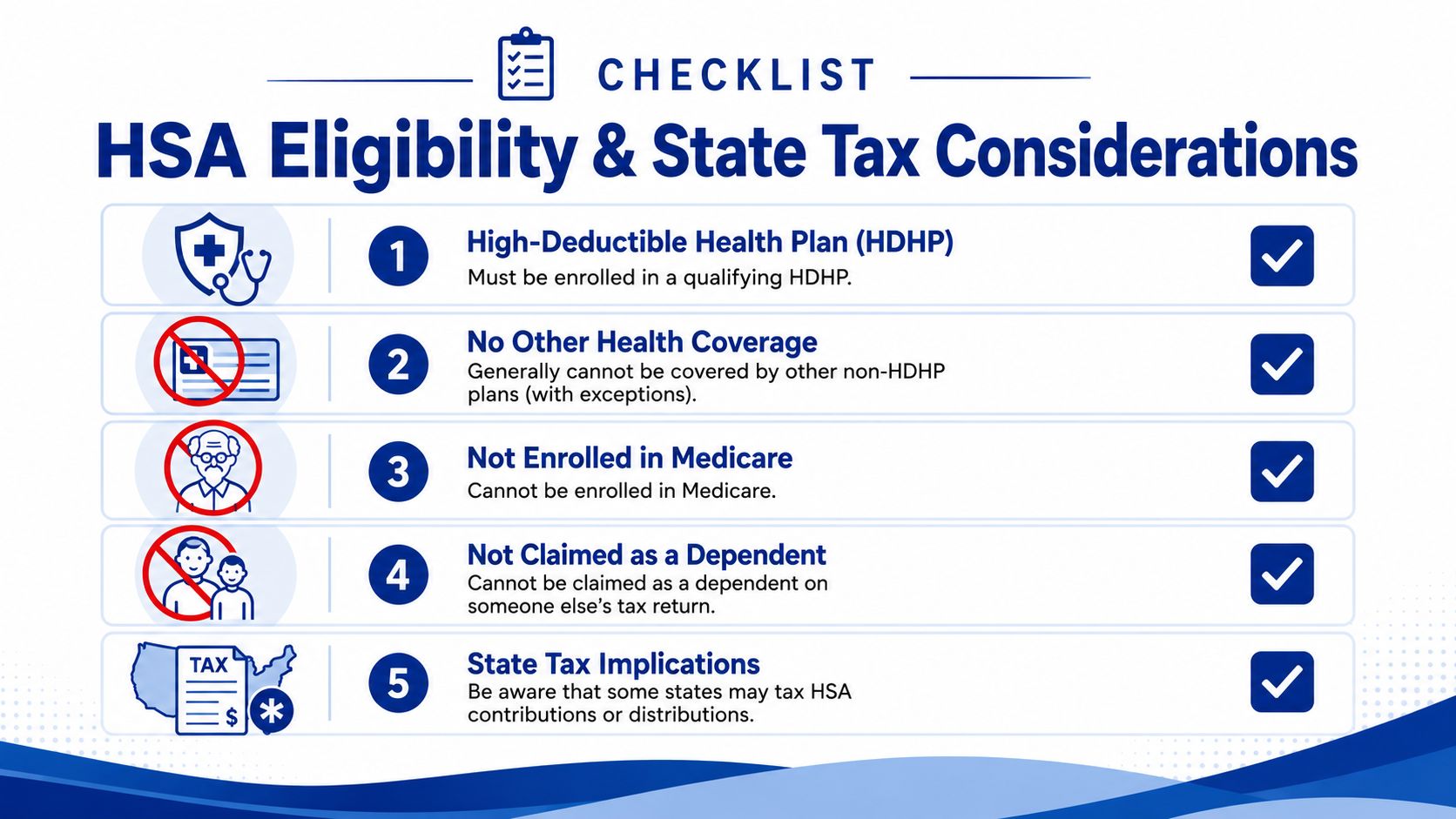

Before any HSA contribution is funded, confirm that the employee is eligible under the tax rules. Employee intent is irrelevant if the coverage setup does not qualify.

For 2026, the employee must be enrolled in an HSA-qualified HDHP that meets the applicable IRS deductible and out-of-pocket requirements discussed earlier in the article. That is only the starting point.

HR and payroll also need to screen for the issues that regularly create contribution errors:

SMBs often get into trouble because the medical election in the HRIS may look correct while the employee's broader coverage situation tells a different story. A good process asks for enough information to catch that mismatch before payroll starts withholding.

Federal tax treatment is only part of the job. State reporting can create employee questions, payroll adjustments, and year-end confusion, especially for employers with remote staff in multiple states.

Some states do not follow the federal HSA tax rules in full. In practice, that can affect state taxable wages, withholding, and the way employees read their pay statements. The federal annual limit does not change, but the employee's state tax result may.

That distinction matters in employee communication. If payroll explains HSA deductions as fully pre-tax without qualifying the state treatment, employees may assume the tax result is identical everywhere they work. For a small employer, that kind of overgeneral message creates avoidable cleanup work.

Employees often ask a different question once money reaches the account. They want to know what the HSA can pay for, including specialty items such as running shoes that accept HSA. That spending question is separate from contribution eligibility. HR teams should keep those topics distinct in notices and enrollment materials.

If the company is reviewing plan design more broadly, this guide to small business benefits packages is a useful reference point. HSA administration works best when plan design, payroll setup, and employee communication are aligned and documented.

Good HSA administration isn't just about knowing the rules. It's about building a process that still works when enrollment changes, payroll staff turns over, or an employee asks for an exception late in the year.

SMBs usually don't need a more complicated system. They need a more disciplined one.

Start with a written internal process, even if the company is small. It should identify who confirms eligibility, who enters payroll deductions, who tracks employer contributions, and who handles correction requests if something goes wrong.

The strongest setups usually include:

The highest-risk HSA situations usually involve a change event. New hire eligibility. A switch in coverage tier. Medicare enrollment. A year-end request to accelerate contributions.

Those aren't moments to rely on memory or verbal advice. They call for a short written record that captures what changed, what rule was applied, and what the employee was told.

A broader review of best staff benefits can help leadership teams think about HSA administration as part of a larger benefits governance issue, not a standalone payroll task.

The companies that handle HSAs well tend to do one thing consistently. They treat contribution administration as a compliance workflow, not just an employee convenience feature.

If your team is dealing with multi-state compliance, sensitive benefits administration issues, or higher-stakes HR decisions that need defensible structure, Paradigm International Inc. can help you evaluate the risk, tighten the process, and support leadership with practical judgment.