Understanding the difference between an independent contractor and an employee is crucial for any business owner. This distinction is not just a matter of payroll; it determines who is in control of the work being performed. While an employee follows your company's direct guidance, an independent contractor operates their own business and provides you with a service. Misinterpreting this relationship is one of the most significant compliance risks a business can face, with serious financial and legal consequences.

Treating worker classification as a simple HR or payroll task is a critical mistake. It is a foundational business risk, and a single misclassification can trigger a chain reaction of liabilities. These issues can put your company’s finances and future in jeopardy, making it a topic that deserves every business leader’s full attention.

The penalties for misclassifying an employee as a contractor are severe and expensive. They frequently include:

A worker's status is not determined by a contract alone. Regulators analyze the economic reality of the relationship, focusing on the degree of control your business exercises over the worker.

This legal landscape is made more complex by a patchwork of federal and state laws. Federal agencies like the Department of Labor (DOL) and the IRS use their own distinct tests to determine a worker’s status. On top of that, many states have introduced even stricter standards, like the "ABC test," which presumes a worker is an employee unless the business can prove otherwise. For businesses operating across state lines, this creates a massive compliance headache. For instance, the distinction has major implications for workers' compensation, as you can see in this breakdown from Lein Law Offices on workers' compensation.

A proactive and well-informed approach is the only defense. Understanding the various legal tests is your first step toward making classification decisions that will hold up under scrutiny.

When federal agencies evaluate your workforce, they focus on one fundamental question: is a worker economically dependent on your business, or are they truly in business for themselves? This is the core of the economic reality test, the primary framework the Department of Labor (DOL) uses to enforce the Fair Labor Standards Act (FLSA). It is designed to look past job titles and contract language to uncover the real nature of the working relationship.

This is not a simple checklist. Instead, regulators weigh several key factors together to get the full picture. How you manage day-to-day work can completely change the outcome, regardless of what your contractor agreement says.

The DOL’s current rule outlines a six-factor framework to guide the Independent Contractor vs. Employee Test. To make a classification decision that holds up under scrutiny, you need to understand how each of these factors is interpreted.

The economic reality test is a totality-of-the-circumstances analysis. No single factor is decisive; regulators weigh all six to determine the true nature of the work relationship. With independent contractors making up a significant portion of the U.S. workforce, regulators are paying close attention. You can explore more details about worker classification from Greenleaf Trust.

Just because a worker passes the Department of Labor's test does not mean you are in the clear. The Internal Revenue Service (IRS) has its own Independent Contractor vs. Employee Test for federal tax purposes. A worker can be classified correctly for labor law but still be considered an employee by the IRS, creating a major compliance issue if you are not careful.

The IRS relies on a common-law test that organizes evidence into three main categories. The agency evaluates the entire working relationship to see how much control your business has over the worker.

To determine a worker's status, the IRS groups the facts of the relationship into three distinct areas. The weight of the evidence across all categories paints the full picture.

A written agreement stating a worker is an independent contractor is not enough to protect you. The IRS will always prioritize the actual facts of the working relationship over the language in a contract.

Because the labor law and tax tests are not identical, the classification can be unclear. In such cases, either the business or the worker can file Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding. This form asks the IRS to review the facts and issue an official determination. While this provides a definitive answer, it also puts a potential misclassification directly on the IRS's radar.

Misclassification can trigger back payroll taxes, overtime liability, and steep penalties. You can find additional details on the IRS worker status page. Understanding both DOL and IRS tests is fundamental, but your classifications must also stand up to state-level scrutiny, which is often stricter.

While federal tests provide a baseline for worker classification, the rules often become more complicated at the state level. Many states have implemented their own, stricter standards. For any business operating across state lines, this patchwork of rules creates a significant compliance challenge. A worker who might pass as a contractor under federal guidelines could be reclassified as an employee under a tough state-level Independent Contractor vs. Employee Test.

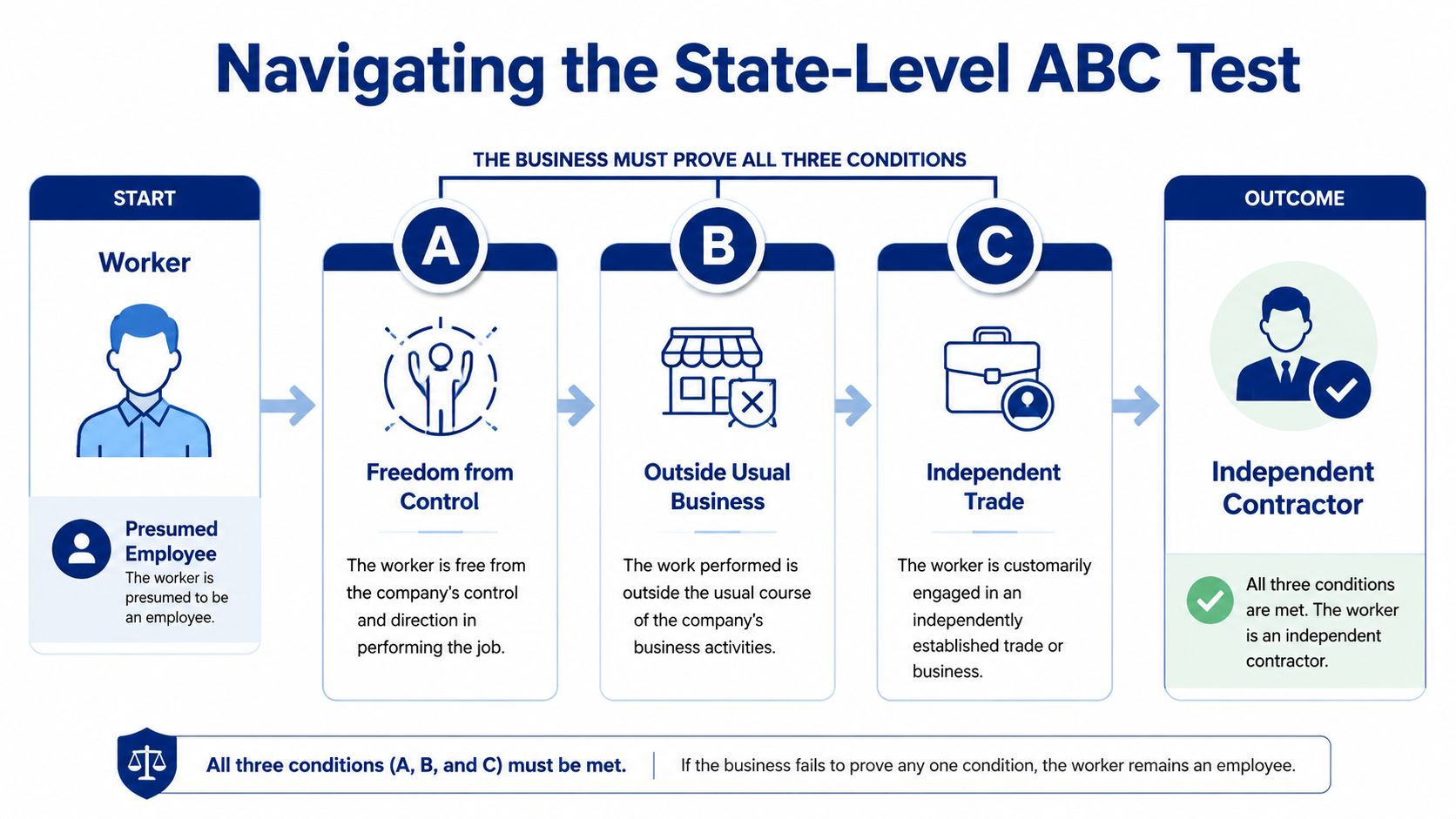

The most challenging of these are the ABC tests, which are now law in states like California and Massachusetts. Unlike federal tests that balance multiple factors, the ABC test is a rigid, all-or-nothing framework. It starts by presuming every worker is an employee, placing the full burden of proof on the business to prove otherwise.

To classify a worker as an independent contractor under an ABC test, you must prove that your working relationship meets all three of the following conditions. If you fail to satisfy even one, the worker is legally considered an employee.

Prong B is often the highest hurdle for businesses to clear. If a tech company hires a software developer or a marketing agency brings on a copywriter, that work is almost always seen as being within the "usual course of business," making contractor status nearly impossible. The UK's IR35 guidance for businesses offers a look at how similar rules impact businesses internationally.

Worker classification standards are not set in stone; they evolve. The federal standard changed significantly when a new Department of Labor rule took effect on March 11, 2024, replacing a different version from 2021. This shifting timeline is critical because federal rules do not override stricter state laws. A classification that was defensible under one framework can easily fail under another, which is why a state-by-state analysis is essential.

Given these complexities, it is vital for leaders to understand the specific laws in every state where they engage workers. Our guide on multi-state remote worker compliance can offer further insights into managing these challenges.

Moving from legal theory to practical application means creating a structured, repeatable process for classifying workers. A defensible classification is not just about the final answer; it is about documenting the why behind your decision before any work begins. This due diligence creates a clear record that can protect your business from future challenges.

An effective framework starts by asking the right questions. What specific state law applies where the work will be performed? How much control will your business have over the worker’s methods? Is their role a core part of what your company offers, or is it a supporting function?

For every independent contractor you engage, you should create a dedicated classification file. Think of this file as your evidence—a paper trail showing you carefully weighed the relationship against the correct legal tests. It is your first and best line of defense if that classification is ever questioned.

A solid classification file should always include these key documents:

The following chart breaks down how to approach a state ABC test, which is an essential analysis for any business engaging workers in states like California.

As you can see, the bar is incredibly high. Failing to satisfy even one of the three requirements automatically results in an employee classification.

Your framework cannot be a one-time exercise. As projects extend or roles change, you must revisit your initial analysis to ensure the classification remains correct. A defensible position is built on consistency. Your daily practices must align with the independent relationship defined in your contract and analysis memo.

This process gives you a concrete, repeatable method for managing classification risk. Proper documentation is also crucial when a working relationship ends, as detailed in our guide on the contractor termination letter. This framework is not about avoiding contractors; it is about engaging them correctly and with confidence.

Getting the Independent Contractor vs. Employee classification wrong has consequences that go far beyond simple paperwork. Misclassification can trigger a chain reaction of financial and operational damage that can jeopardize the health and reputation of your business. These liabilities can be substantial enough to threaten the stability of even a well-established company.

When regulators determine you have misclassified an employee, the financial fallout is immediate and often severe. Agencies like the IRS and Department of Labor will look backward to calculate what you owe.

The potential liabilities can stack up quickly, creating a significant financial burden. Common penalties include:

Proactive compliance is a strategic advantage. It safeguards your business from preventable financial shocks and allows you to build your workforce with confidence. To mitigate this risk, conduct regular audits of your workforce to ensure all classifications remain accurate. Use precisely worded contracts that reflect the true, independent nature of the work relationship. As we detail in our article about employee misclassification penalties, taking these steps is crucial for your protection.

When it comes to the complex world of worker classification, business leaders often have the same recurring questions. A simple misunderstanding of the Independent Contractor vs. Employee Test can expose your company to significant risk. Getting clear, direct answers is the first step toward making confident and defensible workforce decisions. Here, we address some of the most frequent questions we hear.

No. While a well-drafted contract is essential, it is not a silver bullet. Government agencies like the IRS and the Department of Labor will always examine the "economic reality" of the entire work relationship. If your daily practices treat a worker like an employee—by controlling their hours or dictating their methods—a contract declaring them an independent contractor will be invalidated.

The most common and costly error is classifying a worker as a contractor for a role that is permanent, full-time, and integral to the company's core services. This creates an immediate red flag for regulators. For example, a tech company hiring a "freelance" developer to work 40 hours a week on their main product, using a company-provided laptop, is taking a huge misclassification risk.

The substance of the relationship always outweighs the label. If it looks and feels like an employer-employee relationship in practice, regulators will almost certainly see it that way, regardless of your contract.

Yes, absolutely. This is a critical point that many companies with remote workforces overlook. Employment law is governed by the state where the work is physically performed. If you have a remote worker in California, you must analyze that relationship under California's strict ABC test, even if your company is headquartered in a state with a more lenient standard. A one-size-fits-all policy is no longer a defensible strategy.

Navigating these high-stakes decisions requires careful judgment and a clear understanding of both federal and state laws. At Paradigm International Inc., we provide expert guidance to help leadership teams reduce employment risk and maintain defensible HR practices.

If you are ready to ensure your worker classifications are compliant and secure, we invite you to contact us to discuss your specific needs.