You're staring at a payroll report after hiring a few employees, and one line item keeps raising questions. Federal withholding makes sense. Social Security and Medicare are familiar. Then you see SUI and wonder whether it's another employee deduction, a state fee, or something your payroll system added without explanation.

That confusion is common, especially for owners who are building a company while learning payroll rules in real time. SUI isn't just an accounting detail. It affects compliance, budgeting, hiring plans, and how expensive turnover becomes over time. If you operate in more than one state, it can also become a source of avoidable risk.

A clear SUI tax definition helps you make better decisions long before a state agency sends a notice. Once you understand what it is, how it's calculated, and why rates change, the line item stops looking mysterious. It starts looking like what it really is: a manageable business obligation with real strategic consequences.

SUI tax means State Unemployment Insurance. In payroll practice, it refers to a state-level, employer-paid tax that helps finance temporary benefits for workers who lose their jobs through no fault of their own. It's also commonly called SUTA, short for State Unemployment Tax Act. Employers generally must pay both federal and state unemployment taxes if they meet standard coverage thresholds, including paying at least $1,500 in wages in a quarter or having at least one worker during 20 weeks in a calendar year, as outlined in this overview of SUI and employer coverage thresholds.

Think of SUI as a state-managed insurance system funded by employers. When a former employee qualifies for unemployment benefits, the state program provides temporary income support based on that state's rules. Your business contributes to that system through payroll taxes.

That's why the SUI tax definition matters beyond bookkeeping. It connects employment decisions to a public benefits system, and it creates a direct relationship between your workforce practices and a recurring tax cost.

Practical rule: SUI is generally an employer cost, not a standard deduction from employee wages.

Business owners often mix up SUI and FUTA because both relate to unemployment taxes. They are related, but they aren't the same.

SUI is the state unemployment tax. FUTA is the federal unemployment tax framework that supports the broader unemployment system. In day-to-day payroll administration, that means you may owe unemployment-related taxes at both levels, but the state side is the one that usually varies more from one employer to another.

To understand it in a simple way:

| Tax type | Who governs it | Who generally pays it | Main function |

|---|---|---|---|

| SUI | State | Employer | Funds state unemployment benefits |

| FUTA | Federal | Employer | Supports the federal unemployment system and state workforce administration |

If you're running an SMB, SUI isn't a passive background tax. It can shift based on where you hire, how stable your workforce is, and how your terminations are handled. That makes it more like a controllable risk factor than a fixed overhead item.

Owners who understand this early usually make better choices in three areas:

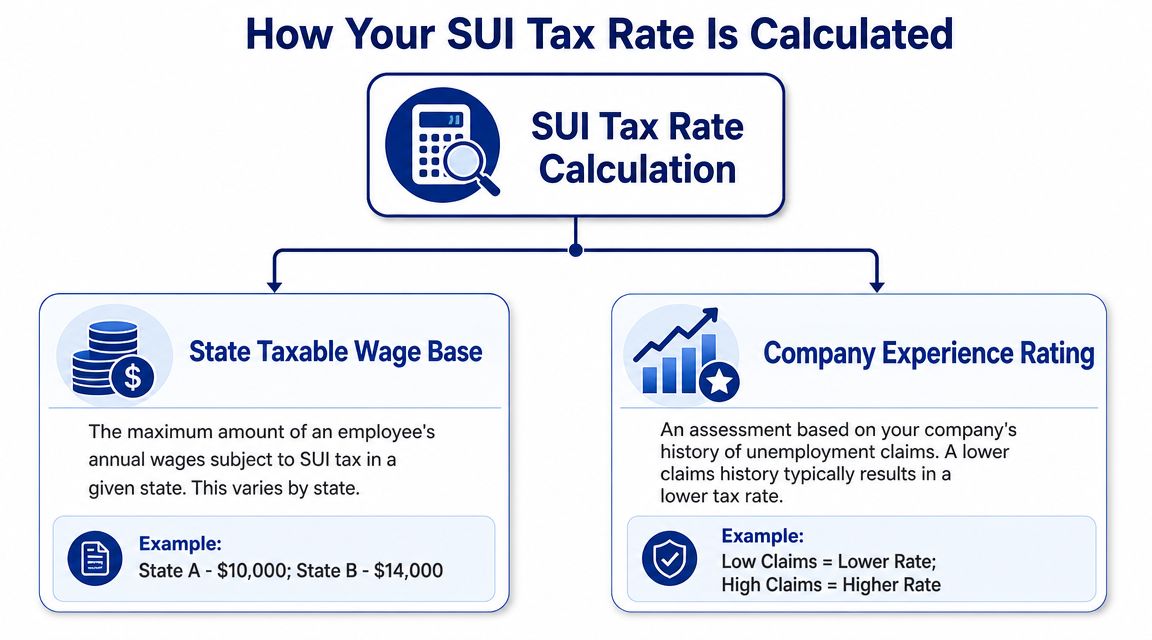

The part that catches many owners off guard is this: SUI usually isn't a flat charge applied to all wages forever. The tax is generally calculated using your assigned SUI rate and only the wages that fall within that state's taxable wage base. As described in this explanation of how SUTA or SUI liability is calculated, the main cost drivers are the employer's experience rating and the state wage-base cap.

At a high level, employers calculate SUI by applying their assigned state rate to taxable wages, not necessarily to every dollar of payroll.

That means two companies with similar headcount can face very different SUI costs. One may have a lower rate or a lower taxable wage base in a given state. Another may have a higher assigned rate because of its claims history.

Here's where the SUI tax definition becomes operational rather than theoretical.

A useful analogy is insurance pricing. If an employer has frequent separations that lead to unemployment claims, the state may view that employer as a higher-cost participant in the system. If claims are limited and the account remains in better standing, the rate may be more favorable.

Many owners assume unemployment tax is just another percentage of payroll. That's where forecasting errors happen.

For example, once an employee's wages exceed the state wage-base cap, that employee may stop generating additional SUI tax for the year in that state. A business with steady, full-year employees may therefore see a different SUI pattern than a business with frequent turnover or a constant stream of new hires.

A rising payroll doesn't always produce a proportional rise in SUI cost. Workforce stability, claim activity, and state wage-base rules often matter more.

If you want to understand your current and future exposure, review these items regularly:

Suppose two businesses each employ the same number of people. One has low turnover, careful hiring, and well-documented separations. The other cycles through staff quickly and rarely contests questionable claims. Even if their payroll totals look similar, their SUI positions can diverge significantly because the underlying risk profile is different.

That's why smart operators treat SUI as an indicator of organizational discipline. Payroll is where the cost appears, but drivers often sit in hiring, management, and documentation.

Most SUI problems don't start with a dramatic audit. They start with missed setup steps, inaccurate reports, or payments sent to the wrong agency. For a new employer, the safest approach is to treat SUI compliance as a repeating workflow: register, report, pay, and reconcile.

Once you hire employees, you generally need a state unemployment account in each applicable state. That registration step matters because the state uses it to assign your account, track wages, and issue your rate notice.

A common mistake is assuming payroll software alone has “handled” registration. Software can help, but the legal obligation still sits with the employer. If your setup is incomplete, the downstream issues usually show up when quarterly reports are due.

States typically require wage reporting on a recurring basis. Those filings often include employee wage data and other identifying information used to calculate tax liability and track benefit eligibility.

Keep your records aligned across payroll, HR, and tax reporting. If your headcount records, worker classifications, and wage reports don't match, the inconsistency can create unnecessary scrutiny. This becomes more serious when the business also has classification issues, which is why leaders should understand the employment risks discussed in this guide to employee misclassification penalties.

Late payments can create a chain reaction. Even when the dollar amount starts small, unresolved issues can grow into notices, penalties, interest, and a broader review of your payroll practices.

A practical compliance rhythm includes:

If a state questions your filings, your best defense is organized records and a consistent reporting trail.

If your team is already dealing with notices or document requests, it helps to understand how states typically approach reviews and disputes. This guidance for state tax audits offers useful context on how tax audit issues can develop and why early response matters.

For most SMBs, the key isn't mastering every state form from memory. It's building a repeatable process that catches errors before they become a regulatory problem.

SUI gets more complicated the moment your workforce crosses state lines. There is no single national SUI rate for employers. The system is state-run, employer-financed, and structured so that states set their own wage bases and rates. At the federal level, the unemployment system commonly references the first $7,000 of wages per employee for federal purposes, while states set their own separate rules. Texas, for example, reports a $9,000 taxable wage base per employee per year and a 2026 entry-level rate of 2.70%, as shown in this U.S. Department of Labor unemployment tax reference.

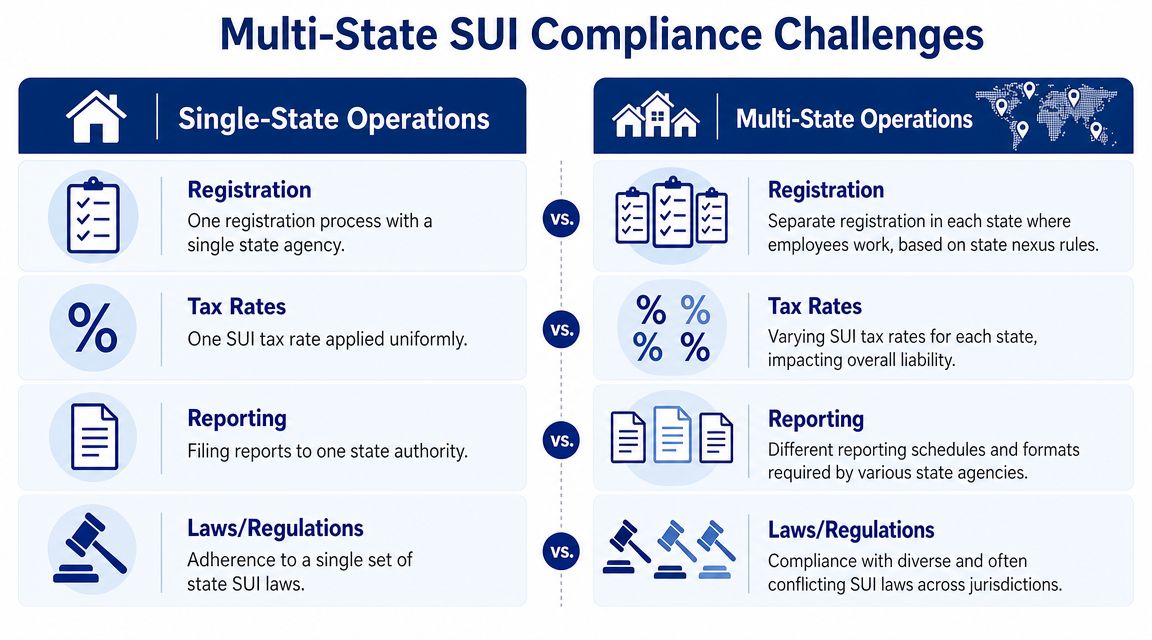

A single-state employer can often build one stable reporting routine. A multi-state employer usually can't.

Different states may require different registrations, different wage bases, different notices, and different interpretations of where wages belong. If your payroll team applies one state's logic to everyone, errors can spread quickly.

Here's the operating contrast:

| Operating model | Compliance picture |

|---|---|

| Single-state workforce | One primary registration path, one state tax environment, fewer assignment questions |

| Multi-state workforce | Multiple state agencies, separate tax setups, and more judgment calls about where wages should be reported |

The hardest part often isn't calculating the tax. It's determining which state should receive the wages for a particular employee.

For employees who work entirely in one state, that decision is usually straightforward. For remote, hybrid, traveling, or regionally managed employees, the issue becomes more fact-specific. Employers often need to evaluate where the work is localized, where the employee is based, and where direction or control occurs under applicable unemployment rules.

That's why multi-state payroll is closely tied to broader labor compliance discipline. Businesses with a distributed workforce should also review their approach to multi-state wage and hour compliance, because wage assignment errors and pay practice errors often travel together.

The most common missteps are operational, not theoretical:

Multi-state SUI compliance is less about tax math and more about getting location decisions right from the start.

If you're planning to hire across states, SUI should be part of expansion planning, not an afterthought. A new state hire can trigger registration obligations, reporting changes, and a different employer cost structure.

This matters for forecasting. It also matters for risk management. When leaders understand where employees are working and document that clearly, they reduce the chance of paying the wrong state, missing required filings, or discovering the problem only after a notice arrives.

You can't eliminate SUI, but you can influence its cost profile. The strongest lever usually isn't a tax tactic. It's disciplined people management.

That's why businesses with solid hiring, documentation, and retention practices often put themselves in a better position over time. Their payroll team isn't constantly cleaning up preventable claims activity, and their leadership team has better visibility into why costs are moving.

When an employee separation happens, the paperwork behind that decision matters. If your managers can't show what happened, when it happened, and how the employee was informed, the business may struggle to respond effectively when unemployment issues arise.

Good documentation usually includes:

Many owners think of retention as a culture issue or recruiting issue. It's also a financial control issue.

Every avoidable separation can create replacement costs, operational disruption, and potential unemployment exposure. If your business constantly backfills the same role, SUI can become one more recurring consequence of a deeper staffing problem.

A practical leadership question is this: are your recurring claims tied to unavoidable business conditions, or are they tied to fixable management patterns?

State notices shouldn't be filed away without review. They affect your tax cost, and they may reflect assumptions or account activity that deserves a second look.

Review each notice with these questions in mind:

Good HR practices don't just reduce friction. They help control a tax cost that many employers wrongly assume is fixed.

As the business grows, don't rely on one payroll manager remembering every deadline and every claim response rule. Build a repeatable process with role clarity, calendar discipline, and documented review points.

If your organization has reached the point where payroll tax administration is consuming leadership time, it may be worth evaluating a more structured approach such as a managed payroll service model that supports consistency and reduces manual exposure.

Usually, no. In standard payroll practice, SUI is generally an employer-paid tax. Employers should still confirm state-specific rules and setup details, especially when operating across multiple jurisdictions.

In most business conversations, yes. The terms are commonly used interchangeably. SUI stands for State Unemployment Insurance, while SUTA refers to the State Unemployment Tax Act framework behind the tax.

Many do once they meet coverage thresholds under unemployment law. Whether a business is covered depends on factors such as wages paid and employment activity, along with state-specific rules.

Because it isn't always a static payroll expense. State rules, wage-base limits, claims activity, account history, and business changes can all affect what you owe.

Yes. Business acquisitions can affect tax accounts, assigned rates, reporting responsibilities, and how prior employment history is treated. This is one of the moments when owners should slow down and verify assumptions before payroll transitions go live.

Yes, although the rules can differ. Some nonprofit employers may fall under alternative unemployment funding approaches depending on state law and organizational status. The key point is that exemption assumptions should never be made casually.

That can change which state should receive unemployment wages. Remote work often creates assignment questions that aren't obvious from the employee's job title alone. Employers should document where the work is performed and confirm that payroll reporting matches those facts.

They treat it as a passive payroll line instead of an active compliance and risk issue. When that happens, leaders miss early warning signs in turnover, documentation quality, and multi-state setup.

If your team is facing complex workforce changes, uncertain state assignments, or sensitive employment decisions, it often helps to get experienced outside perspective before a minor issue becomes a larger one.

If your leadership team wants help navigating employment risk, multi-state compliance questions, or defensible people decisions, Paradigm International Inc. offers advisory support built for growing businesses that need clear judgment and practical structure.